Depreciation Accounting for Bankers: JAIIB AFM Made Simple 2026

Depreciation accounting is one of the most reliably tested numerical areas in the JAIIB AFM paper, and the good news is that the calculations follow a small number of fixed patterns. Once you understand why depreciation accounting exists and how the two main methods behave, the numericals become quick marks. This guide walks through the concept, the methods, the journal entries and the exam shortcuts.

Why Depreciation Exists

Depreciation accounting is the systematic allocation of the cost of a fixed asset over its useful life. A bank that buys an ATM or a building does not expense the entire cost in year one; instead it spreads the cost across the years that benefit from the asset, matching cost with revenue. This is a direct application of the matching principle and the going concern assumption.

Three factors determine the charge: the cost of the asset (including installation), the estimated useful life, and the expected residual or scrap value. The depreciable amount is cost minus residual value. Candidates should be clear that depreciation is a non-cash expense — it reduces book profit but involves no cash outflow, which is why it is added back when preparing a cash flow statement. The accounting standards underpinning depreciation accounting are issued by the Institute of Chartered Accountants of India. Practise these fundamentals on our AFM numerical tests.

Straight Line Method (SLM)

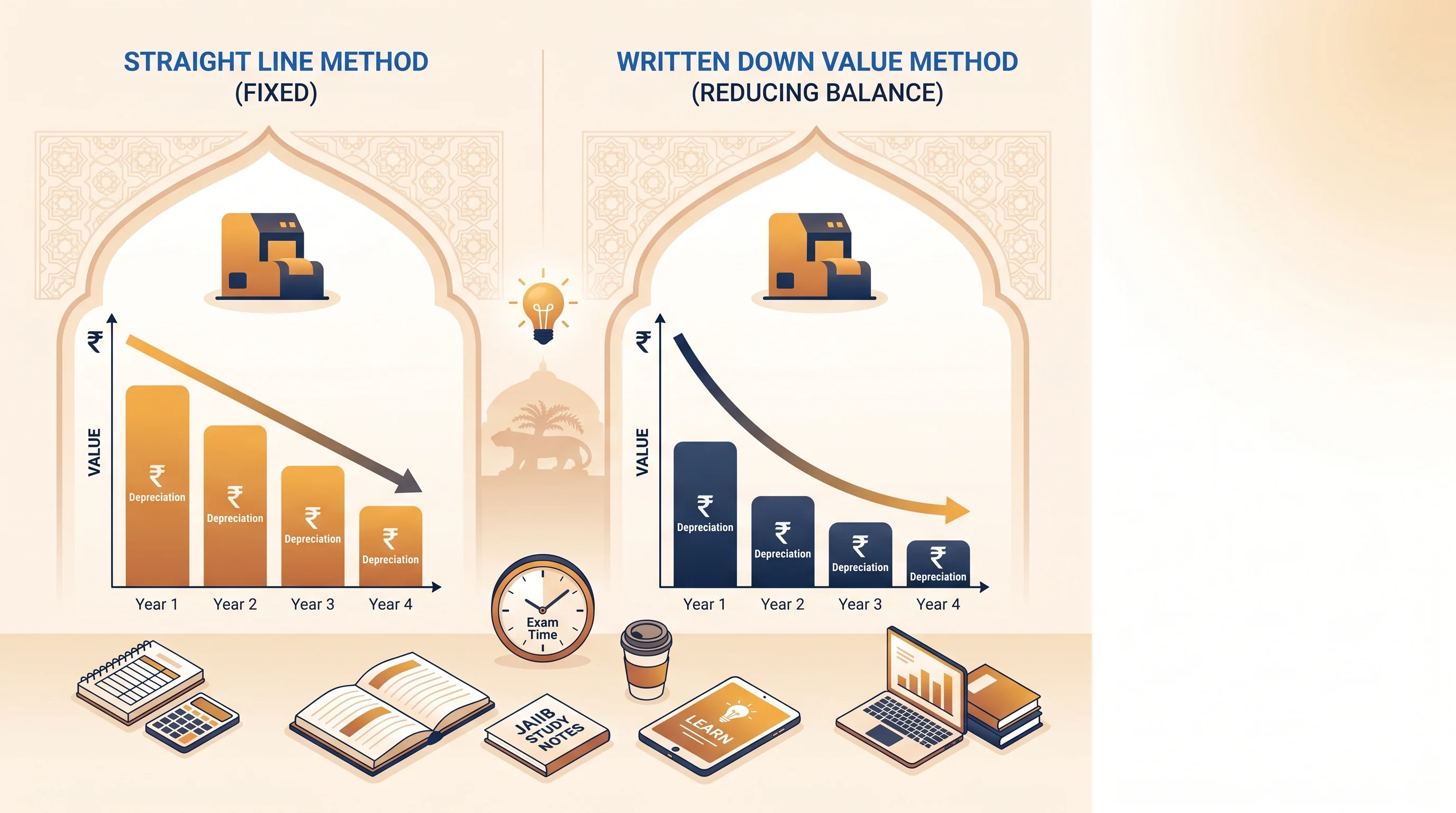

Under the Straight Line Method, an equal amount of depreciation is charged every year. The formula is (Cost − Residual Value) ÷ Useful Life. If a machine costs Rs 1,00,000, has a residual value of Rs 10,000 and a life of nine years, annual depreciation is (1,00,000 − 10,000) ÷ 9 = Rs 10,000 every year. The book value declines in a straight line until it reaches the residual value.

SLM suits assets that give uniform service, such as buildings and furniture. Its advantage is simplicity, and the rate as a percentage of original cost stays constant. A common variant asks you to compute the depreciation rate: divide annual depreciation by original cost and express it as a percentage. Watch whether the question gives the rate or the life, because mixing them up is the single most common error in depreciation accounting. Reinforce the formula with our accounting concepts match game.

Written Down Value Method (WDV)

The Written Down Value or reducing-balance method applies a fixed percentage to the opening book value each year, so the charge is highest in year one and falls thereafter. If an asset costs Rs 1,00,000 and the WDV rate is 20%, year-one depreciation is Rs 20,000 (book value Rs 80,000), year two is Rs 16,000 (book value Rs 64,000), and so on. The asset is never fully written off to zero under pure WDV.

WDV suits assets like vehicles and computers that lose more value early and incur higher repairs later, so depreciation plus repairs stays more even. For exams, remember the contrast: SLM gives equal depreciation but a rising proportion relative to book value, while WDV gives falling depreciation but a constant rate on book value. Indian income-tax depreciation largely follows the block-of-assets WDV approach, a fact examiners slip into theory questions. Lock in both methods with a full JAIIB AFM module.

Journal Entries and Exam Shortcuts

The standard entry debits the Depreciation Account and credits either the Asset Account directly or a Provision for Depreciation (Accumulated Depreciation) Account. At year-end, Depreciation A/c is transferred to the Profit and Loss Account. When the asset is sold, compare sale proceeds with the written-down value to compute profit or loss on sale — a favourite multi-step numerical in depreciation accounting.

For speed, memorise that under SLM the annual figure repeats, so once you compute year one you can multiply for accumulated depreciation. Under WDV, build a quick table rather than forcing a single formula. Always check the date of purchase: an asset bought mid-year is depreciated only for the months in use. These small disciplines convert tricky three-mark questions into easy ones. Stay sharp on the latest exam pattern through our IIBF updates page.

Exam Strategy and Quick Revision

To master depreciation accounting, drill both methods until the tables come automatically, and keep a checklist for every numerical: cost including installation, residual value, useful life or rate, and date of purchase. Most errors come from missing one of these inputs, not from the arithmetic.

In the final week, practise mixed numericals that combine depreciation with sale of an asset, since these test several skills at once. Attempt full mocks under timed conditions and review every slip. Combine this disciplined practice with our timed AFM mock tests and the worked examples on our study blog, and you will bank these marks every time.

What is the difference between SLM and WDV depreciation?

SLM charges an equal amount each year on the original cost, while WDV applies a fixed percentage to the reducing book value, so depreciation is higher early and falls over time.

Why is depreciation added back in the cash flow statement?

Because it is a non-cash expense. It reduces book profit but involves no cash outflow, so it is added back to net profit when computing cash from operations.

How is the depreciable amount calculated?

Depreciable amount equals cost of the asset (including installation) minus its estimated residual or scrap value, allocated over the asset's useful life.

Which method does Indian income tax generally use?

Indian income tax largely uses the written down value method under a block-of-assets approach, grouping assets of the same class and rate together.

Common Pitfalls and Final Tips

A frequent mistake in the JAIIB AFM paper is memorising rules without being able to apply them to a scenario. Examiners often wrap the SLM and WDV formulas, the journal entries and the profit-or-loss-on-sale numerical inside a short case, so practise translating each concept into a worked example rather than reciting it. Another common slip is confusing closely related terms, so keep a running list of easily-mixed concepts and test yourself on the distinctions until they are automatic.

In the final week, prioritise active recall over passive reading: attempt full-length mocks under timed conditions, review every incorrect answer, and revisit only the topics where you stumble. Manage the clock carefully in the exam hall by flagging difficult questions and returning to them rather than losing momentum on a single item. Read each question stem twice, since negatively-phrased options such as "which is NOT" trip up even well-prepared candidates.

Finally, link your study to current developments, because the exam increasingly tests recent regulatory changes alongside core theory. Combine this disciplined approach with our timed JAIIB AFM mock tests, the quick-revision match games and the detailed explainers on our study blog, and you will walk into the exam confident and well-prepared.

Conclusion

Depreciation accounting rewards practice more than theory. Understand the matching principle, drill SLM and WDV, and never forget to check the purchase date and residual value. Put it together with a timed AFM mock test and you will secure these marks. For a structured revision plan, enrol in our JAIIB course.

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.