NBFC Regulation in India: Scale-Based Framework for IIBF 2026

NBFC Regulation in India: The Scale-Based Framework Explained for IIBF 2026

NBFC regulation in India has been completely reshaped by the Reserve Bank of India's move to a scale-based framework, and the IIBF NBFC paper now tests this architecture in granular detail. A Non-Banking Financial Company delivers banking-like credit, investment and leasing services without holding a full banking licence, reaching customers and segments that traditional banks frequently overlook. If you are preparing for the IIBF NBFC certificate examination in 2026, mastering how these institutions are defined, classified and supervised is the single highest-yield investment you can make in your study plan.

This guide walks you through the complete regulatory picture: what an NBFC actually is, the principal business criterion the RBI uses to bring a company under its net, the four-layer Scale-Based Regulation (SBR) structure, the activity-based categories, co-lending, harmonised NPA norms, and exactly how an NBFC differs from a bank. Everything is framed for the exam, with worked angles and revision hooks so you can convert understanding into marks.

Key Takeaways

- An NBFC lends and invests but cannot accept demand deposits, issue cheques on itself, or offer DICGC deposit insurance.

- The principal business criterion brings a company under RBI's NBFC net when financial assets exceed 50% of total assets and financial income exceeds 50% of gross income.

- Scale-Based Regulation (SBR) sorts NBFCs into four layers — Base, Middle, Upper and a normally-empty Top Layer — with rules tightening as you move up.

- Activity-based types include ICC, IFC, IDF, MFI, Factor, CIC, HFC and P2P platforms, each defined by what it does.

- NPA recognition has been harmonised towards the 90-day overdue norm that applies to banks.

What Is an NBFC? The Definition That Anchors the Paper

An NBFC is a company registered under the Companies Act whose principal business is lending, investment in shares and securities, leasing, hire-purchase or insurance — but which is not a bank. This distinction matters because the entire regulatory edifice rests on it. NBFC regulation in India deliberately treats these companies differently from banks precisely because their funding model, risk profile and customer reach are different.

To decide whether a company needs NBFC registration, the RBI applies a principal business criterion. Broadly, financial assets must be more than 50% of total assets, and financial income must be more than 50% of gross income. Only when both legs of this test are satisfied does a company fall within the definition and require registration with the Reserve Bank. This "50-50 test" is a perennial favourite of examiners, so commit it to memory and be ready to apply it to a numerical scenario.

Crucially, an NBFC cannot accept demand deposits the way a bank does, is not part of the country's payment and settlement system, and depositors with an NBFC do not enjoy deposit insurance from the DICGC. These three limitations define the boundary between a finance company and a bank, and they reappear throughout the syllabus.

Deposit-Taking Versus Non-Deposit NBFCs

NBFCs are first sorted by their liability structure. A deposit-taking NBFC (NBFC-D) is permitted to accept public deposits within prescribed limits and therefore faces stricter prudential supervision. A non-deposit-taking NBFC (NBFC-ND) funds itself through borrowings, bonds and equity rather than public deposits.

Within the non-deposit universe, the larger entities are designated systemically important because their failure could ripple through the wider financial system. This systemic-importance lens is the conceptual seed from which the entire Scale-Based Regulation framework grew, so understanding it here pays off later.

Types of NBFC by Activity

Beyond their liability structure, NBFCs are classified by the activity they carry out — and matching each type to its defining activity is one of the most common question formats in the exam. The broad workhorse category is the Investment and Credit Company (NBFC-ICC), which now covers asset finance, loans and investments after several earlier sub-categories were merged into a single label.

The specialised categories each have a sharp, examinable definition:

- Infrastructure Finance Company (IFC) — deploys the bulk of its assets into infrastructure loans.

- Infrastructure Debt Fund (IDF) — channels long-term funds into infrastructure projects.

- NBFC-Microfinance Institution (NBFC-MFI) — serves low-income and unbanked borrowers with small-ticket credit.

- NBFC-Factor — specialises in receivables financing and factoring.

- Core Investment Company (CIC) — holds investments in group companies rather than lending to the public.

- Housing Finance Company (HFC) — finances home loans and is now regulated by the RBI.

- Peer-to-Peer (P2P) lending platform — connects individual lenders and borrowers directly, without lending from its own books.

For the exam, do not just recognise these names — be able to pick the right type from a one-line description of its business. You can drill exactly this skill in the NBFC types matching game, which turns rote definitions into fast recall.

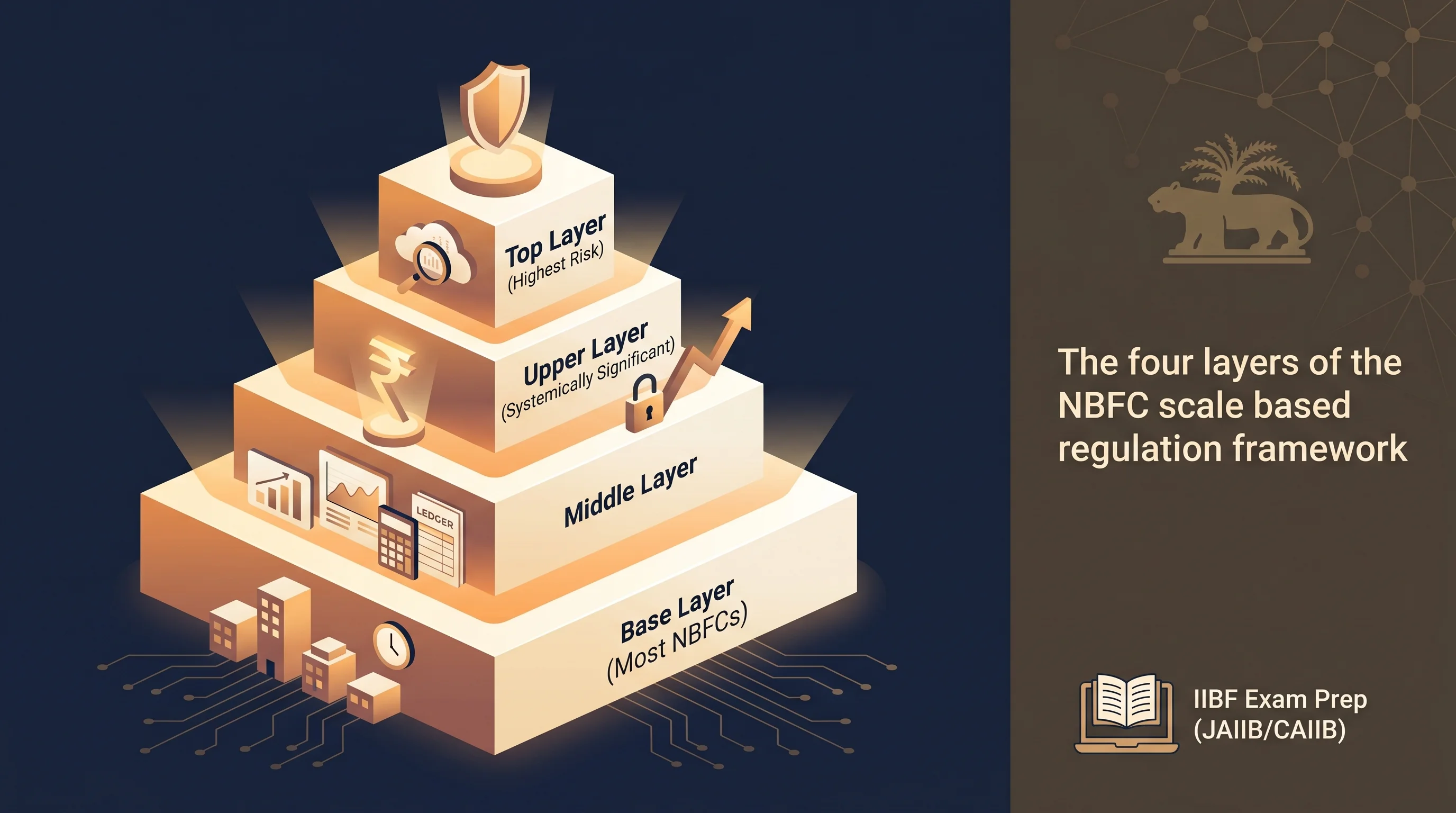

The Scale-Based Regulation (SBR) Framework

NBFC regulation in India took a decisive turn when the RBI introduced Scale-Based Regulation, recognising that a tiny non-deposit NBFC and a large systemically important one should never face an identical rulebook. The framework places every NBFC into one of four layers, with the intensity of supervision rising as you climb.

| Layer | Who Sits Here | Regulatory Intensity |

|---|---|---|

| Base Layer (NBFC-BL) | Smaller non-deposit NBFCs, P2P platforms and similar | Lightest regulation |

| Middle Layer (NBFC-ML) | Deposit-taking NBFCs and larger non-deposit ones | Moderate, with tighter prudential norms |

| Upper Layer (NBFC-UL) | Most systemically significant NBFCs, identified by the RBI | Bank-like norms, leverage ceiling, enhanced governance |

| Top Layer | Normally empty | Activated only if an NBFC poses extreme systemic risk |

The Base Layer carries the lightest touch and houses smaller non-deposit NBFCs. The Middle Layer captures deposit-taking NBFCs along with larger non-deposit entities. The Upper Layer comprises the most systemically significant NBFCs, hand-picked by the RBI and subjected to bank-like prudential norms — including a leverage ceiling and enhanced governance expectations. The Top Layer deliberately remains empty unless the regulator judges that a specific NBFC poses extreme systemic risk, at which point it can be moved up.

For a deeper, layer-by-layer treatment with the supporting norms, work through our dedicated explainer on the NBFC Scale-Based Regulation: the RBI SBR framework, and pair it with the focused Scale Based Regulation IIBF exam guide. The precise figures and thresholds that decide layer placement are revised periodically, so always confirm the current numbers against the latest released IIBF notification and the official RBI master direction.

Co-Lending, NPA Norms and the Bank Comparison

NBFCs increasingly partner with banks through the co-lending model, in which a bank and an NBFC jointly fund a single loan to priority-sector borrowers. The arrangement marries the bank's low-cost funds with the NBFC's last-mile reach, expanding credit to segments neither could serve as efficiently alone. Co-lending is a high-frequency exam topic — understand who contributes what, and why the model exists.

On the prudential side, the RBI has steadily tightened NBFC norms. Most notably, the NPA recognition timeline has been harmonised towards the 90-day overdue norm that already applies to banks, accompanied by stricter provisioning and governance requirements. Liquidity and asset-liability mismatches have triggered NBFC stress episodes in the past, prompting the introduction of a liquidity coverage ratio (LCR) for larger NBFCs to ensure they hold enough high-quality liquid assets.

Despite this convergence, the core difference from a bank endures: an NBFC cannot issue cheques drawn on itself, cannot accept demand deposits, and offers no deposit insurance — yet it often lends faster and reaches niche segments more effectively. The table below crystallises the comparison.

| Feature | Bank | NBFC |

|---|---|---|

| Demand deposits | Can accept | Cannot accept |

| Cheques drawn on itself | Yes | No |

| Payment & settlement system | Part of it | Not part of it |

| Deposit insurance (DICGC) | Available | Not available |

For a focused treatment of how these pieces interconnect, our guide on co-lending and P2P lending under the RBI model and FLDG is essential reading, and the layers, NPA norms and co-lending explainer ties the prudential threads together.

A Practical Study Plan for the NBFC Paper

Knowing the syllabus is one thing; converting it into a confident exam performance is another. Here is a structured, four-week approach that has worked for thousands of Learning Sessions candidates.

- Week 1 — Build the skeleton. Lock down the NBFC definition, the principal business criterion, and the NBFC-D versus NBFC-ND split. Read the official scope of NBFC supervision directly from IIBF's official site so your foundation matches the source.

- Week 2 — Master the two frameworks. Memorise the activity-based types (ICC, IFC, IDF, MFI, Factor, CIC, HFC, P2P) and the four-layer SBR structure until you can reproduce both from a blank page.

- Week 3 — Apply, don't recite. Move to scenario practice. Take timed mock tests on the NBFC mock test series and review every wrong answer the same day.

- Week 4 — Sharpen recall and current affairs. Use the matching games for rapid revision and skim the latest guides in our complete NBFC guide library for recent regulatory changes.

Throughout, anchor your reading to the structured curriculum on the NBFC certificate course hub, which sequences these topics in the order the examiner expects you to know them. If you want the full syllabus on paper, the NBFC certificate course syllabus 2026 with free PDF is the fastest way to map your coverage.

Common Mistakes Candidates Make

Tip: The examiner rarely asks a bare definition. Expect concepts wrapped inside a short case, so practise translating every rule into a worked example.

- Memorising without applying. Reciting the four layers is useless if you cannot place a described NBFC into the correct one. Always practise on scenarios.

- Confusing look-alike categories. ICC, IFC and IDF sound similar but serve different purposes. Keep a running list of easily-mixed terms and test yourself until the distinctions are automatic.

- Missing negatively-phrased stems. Options framed as "which is NOT" trip up even strong candidates. Read each stem twice before answering.

- Ignoring current developments. The paper increasingly tests recent regulatory changes alongside core theory, so blend current affairs into your revision rather than treating it as optional.

- Poor clock management. Flag tough questions and return to them rather than bleeding minutes on a single item.

Frequently Asked Questions

How does an NBFC differ from a bank?

An NBFC cannot accept demand deposits and cannot issue cheques drawn on itself. It is not part of the payment and settlement system, and its deposits are not covered by DICGC insurance. Banks enjoy all of these features, which is the fundamental distinction the exam tests.

What are the four layers of scale-based regulation?

The four layers are the Base Layer, the Middle Layer, the Upper Layer and a normally-empty Top Layer. Regulatory intensity increases as you move up the layers. The Top Layer is activated only if the RBI judges that a specific NBFC poses extreme systemic risk.

What is the principal business criterion?

It is the "50-50 test" the RBI uses to decide whether a company is an NBFC. A company qualifies when its financial assets exceed 50% of total assets and its financial income exceeds 50% of gross income. Both conditions must be satisfied for registration to be required.

What is the co-lending model?

Co-lending is an arrangement where a bank and an NBFC jointly fund a single loan, usually to priority-sector borrowers. It combines the bank's low-cost funds with the NBFC's last-mile reach. The model expands credit access to underserved segments more efficiently than either party could alone.

Which NPA norm applies to NBFCs now?

NBFC NPA recognition has been harmonised towards the 90-day overdue norm that already applies to banks. This was accompanied by stricter provisioning and governance requirements. Always confirm the exact implementation timeline against the latest RBI master direction and IIBF notification.

How should I prepare for the IIBF NBFC paper in 2026?

Build the definitions first, then master the activity-based types and the four-layer SBR framework, and finally shift to timed scenario practice. Review every incorrect mock answer and weave recent regulatory changes into your revision. Confirm all time-sensitive specifics, such as exam dates, on the official IIBF notification before relying on them.

Conclusion

NBFC regulation in India blends genuine innovation in credit delivery with steadily rising regulatory rigour through scale-based regulation. Once you can fluently reproduce the principal business criterion, the activity-based types, the four-layer framework and the bank-versus-NBFC differences, this paper transforms from intimidating to dependable. Treat each concept as a tool to apply, not a line to recite, and reinforce it with regular timed mocks.

You already have everything you need to score well — a clear map of the syllabus, a week-by-week plan, and the practice tools to make recall automatic. Put in the focused reps, confirm every date and figure against the official IIBF notification, and walk into the exam hall knowing the NBFC paper is yours to win.

Related Guides

📚 Free Learning Sessions resources — connect & crack your exam

- 📝 Free mock tests — chapter-wise, exam-pattern, with instant solutions

- 🎮 Matching games — gamified revision of key terms & concepts

- 📄 Study notes & PDFs — downloadable chapter material

- 🎥 Video classes on YouTube — subscribe to @learningsessions

💬 Want the full course? WhatsApp your course name to 8360944207 and our team will set you up.

📱 Study on the go — get our iOS & Android app at iibf.store/app.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.