CAIIB ABFM Working Capital Management: Module B Guide

CAIIB ABFM working capital management is the single most rewarding topic in Module B of the Advanced Business and Financial Management paper, because it tests the exact judgement a banker uses every day: how much short-term finance a business genuinely needs, and how safely a bank can lend it. Master the operating cycle, the MPBF and Turnover methods, and the cash-conversion logic, and you will not only clear this section comfortably, you will appraise a working-capital proposal more confidently than most of your peers on the credit desk.

This guide walks through everything ABFM Module B expects on working capital in plain working-banker language. Wherever the syllabus or thresholds are time-sensitive, treat the numbers here as illustrative and confirm the operative figures against the latest IIBF notification and the current RBI master directions before relying on them in the exam hall or at the branch.

Key Takeaways

- Working capital management in CAIIB ABFM revolves around the operating cycle — the days between buying raw material and collecting cash.

- Two assessment families dominate: the MPBF methods (Tandon Committee) for larger limits and the Turnover Method (Nayak Committee) for smaller borrowers.

- The Cash Conversion Cycle (DIO + DSO − DPO) is simply the operating cycle viewed from a cash standpoint; a shorter cycle frees up funds.

- Supporting tools — EOQ, ABC, VED, JIT, factoring and cash-management models — are tested as plug-and-chug or identification questions.

- Expect at least one numerical MPBF or operating-cycle calculation in almost every ABFM paper, so drill the formulas until they are automatic.

Why working capital management dominates ABFM Module B

Working capital is what keeps the lights on at every operating business — wages get paid, raw material is bought, and stock sits on shelves long before a single customer settles an invoice. Module B of CAIIB ABFM devotes a large slice of its mark weight to teaching bankers how to assess, structure and monitor this short-term funding need.

The reason is practical. A term loan funds an asset that you can see and value; working-capital finance funds an invisible, constantly churning gap. Getting that assessment wrong either starves a healthy business of cash or over-finances a weak one. That is why the examiners keep coming back to this chapter — and why a confident grasp of it pays off long after the result is out.

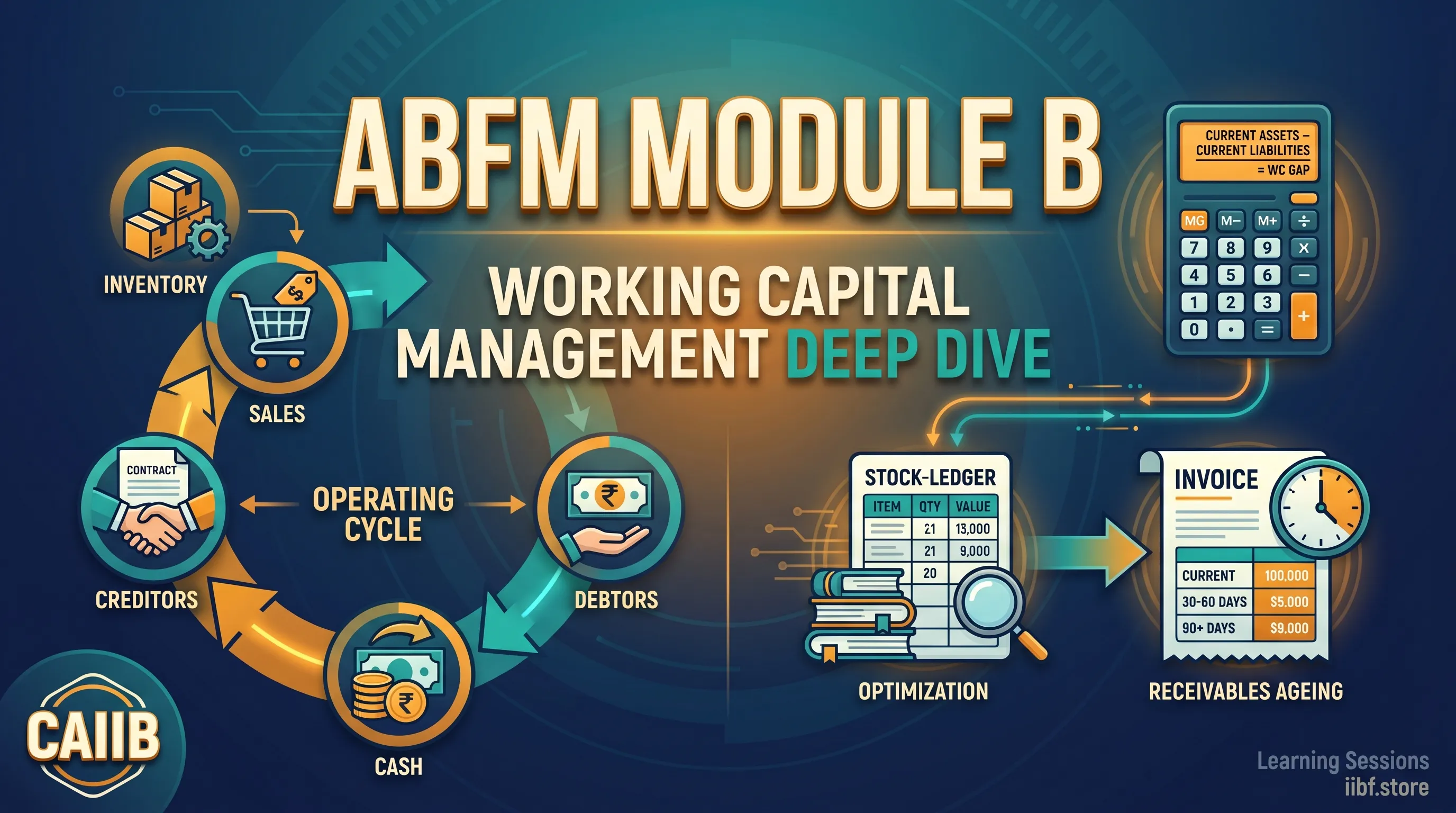

The operating cycle — the foundation concept

The operating cycle is the time it takes for one rupee invested in raw material to return as cash from a customer payment. Everything else in this topic builds on it. For a typical manufacturing unit:

Operating Cycle = Raw Material Holding Period + Work-in-Progress Period + Finished Goods Holding Period + Debtor Collection Period − Creditor Payment Period

Each component has a clean formula you should be able to write from memory:

- Raw Material Holding Period = Average RM stock × 365 ÷ Annual RM consumption

- WIP Period = Average WIP × 365 ÷ Annual cost of production

- Finished Goods Period = Average FG × 365 ÷ Annual cost of goods sold

- Debtor Period = Average debtors × 365 ÷ Annual credit sales

- Creditor Period = Average creditors × 365 ÷ Annual credit purchases

Worked example. A small unit holds 30 days of raw material, takes 15 days to convert it to finished goods, holds finished goods for 20 days, gets paid in 45 days, and itself pays suppliers in 30 days. The operating cycle works out to 30 + 15 + 20 + 45 − 30 = 80 days.

That 80-day cycle means the firm has roughly 80 days of operations to fund at any time. If annual turnover is around three crore rupees, daily turnover is about 0.82 lakh, so the indicative working-capital need is 80 × 0.82 ≈ 66 lakh rupees. This single chain of logic — cycle in days, then rupees — is the spine of the whole topic.

Working capital gap and the MPBF methods

RBI's Tandon Committee (1974) introduced the Permissible Bank Finance framework, later refined into the Maximum Permissible Bank Finance (MPBF). Two methods, often labelled Method I and Method II, are routinely tested in ABFM.

- Method I: Bank finance = 75% of (Current Assets − Current Liabilities other than bank borrowings). The borrower contributes the remaining 25% of the working-capital gap as net working capital.

- Method II: The borrower contributes 25% of total current assets as net working capital, and the bank finances the rest.

Method II is the more conservative of the two because it demands a higher borrower contribution. The exam loves the instruction "calculate MPBF," so drill both formulas until they are second nature.

Worked example (Method II).

- Total current assets: 100 lakh

- Current liabilities excluding bank borrowings: 20 lakh

- Working capital gap (CA − CL) = 80 lakh

- Borrower's contribution = 25% of CA = 25 lakh

- MPBF = Working Capital Gap − Borrower Contribution = 80 − 25 = 55 lakh

Notice how the contribution base differs between the two methods — gap-based in Method I, total-current-assets-based in Method II. Mixing those bases is the most common silly error in this calculation, so read the question stem carefully before you start. For the wider credit framework these methods sit within, the NPA management and recovery guide for CAIIB ABM is a useful companion read.

The Turnover Method (Nayak Committee)

For smaller borrowers, RBI's Nayak Committee recommended a far simpler Turnover Method, historically applied to aggregate working-capital limits up to a prescribed ceiling. Always confirm the current operative threshold against the latest RBI master direction, as it has been revised over time.

Working Capital Limit = 20% of projected annual turnover, with the borrower's margin contribution at 5% of turnover.

The 20% figure broadly assumes a turnover that rotates a few times a year, which is why the method works well for trading and small manufacturing units. Its great virtue is computational simplicity, and that simplicity is exactly why it dominates working-capital sanctions in the micro and small enterprise segment.

Worked example. A small enterprise projects two crore rupees of turnover next year. Sanction limit = 20% × 2 crore = 40 lakh. Borrower contribution = 5% × 2 crore = 10 lakh. Bank finance = 40 − 10 = 30 lakh. Three lines, and you have the answer — which is precisely why examiners and branch managers both like it.

The Cash Conversion Cycle (CCC)

The Cash Conversion Cycle measures the number of days between when a firm pays its supplier and when it receives cash from the customer for the corresponding sale. In substance it is the operating cycle viewed purely in cash terms:

CCC = DIO + DSO − DPO

Here DIO is Days Inventory Outstanding, DSO is Days Sales Outstanding (debtor days), and DPO is Days Payable Outstanding (creditor days). A shorter CCC means faster cash turnover, lower working-capital intensity and a higher return on capital employed.

A firm can even run a negative CCC — collecting cash from customers before it pays its suppliers. This is common in organised retail, where sales are largely on the spot but suppliers extend long credit; in effect the suppliers finance the retailer's working capital. Recognising this pattern is a favourite conceptual question in ABFM.

Inventory management techniques

Module B expects familiarity with four inventory tools, mostly tested as formula or identification questions:

- EOQ (Economic Order Quantity) = √(2 × Annual Demand × Order Cost ÷ Carrying Cost per unit per year). It is the order quantity that minimises total inventory cost.

- ABC Analysis — categorises items by value: A (high-value, tight control), B (medium-value, moderate control), C (low-value, loose control).

- VED Analysis — Vital, Essential, Desirable — used mainly for spare parts and critical manufacturing inputs.

- JIT (Just-in-Time) — minimal inventory with deliveries timed to production; Toyota's Kanban system is the classic example.

For the exam, focus on recognising which technique answers which need — value-based control (ABC), criticality-based control (VED), order sizing (EOQ) and inventory minimisation (JIT).

Receivables management

Receivables management turns on three levers:

- Credit policy — the credit terms offered, such as net 30 or "2/10 net 30," meaning a 2% discount for payment within 10 days and full payment by day 30.

- Collection policy — how firmly and how soon follow-ups are pursued, and when the matter is escalated.

- Factoring and bill discounting — selling receivables to a factor at a discount to monetise them immediately, on either a recourse or non-recourse basis.

The central trade-off is straightforward: tighter credit terms shorten DSO but may cost you sales, while looser terms boost sales but stretch working capital. The art of receivables management is finding the point that maximises profit, not just sales.

Cash management

The final building block is cash management, where a handful of concepts recur in ABFM:

- Cash budget — a month-by-month projection of cash inflows and outflows, and the basis for all short-term working-capital planning.

- Float management — the gap between book cash and bank cash caused by cheques in transit. Modern UPI and IMPS shrink float to almost nothing, though it still matters for cheque-heavy segments.

- Baumol and Miller-Orr models — frameworks for determining the optimal cash balance; these usually appear as "which model determines the optimal cash level?" identification questions.

- Sweep accounts — automatic transfer of surplus cash into interest-earning instruments, and back when needed.

Quick comparison: MPBF vs Turnover Method

The fastest way to avoid mixing up the two assessment families is to hold them side by side. Keep this table in your revision notes.

| Basis | MPBF Methods (Tandon) | Turnover Method (Nayak) |

|---|---|---|

| Typical borrower | Larger limits, structured proposals | Micro and small enterprises |

| Core driver | Current assets and current liabilities | Projected annual turnover |

| Bank finance | 75% of WC gap (I) / CA less 25% margin (II) | 20% of turnover |

| Borrower margin | 25% (of gap or of CA) | 5% of turnover |

| Complexity | Moderate; needs full CMA data | Very low; one line of arithmetic |

A practical study plan for this topic

You can lock down working capital management for ABFM Module B in about a week of focused effort if you sequence it well:

- Day 1-2: Internalise the operating-cycle formula and run five numerical examples until the days-to-rupees conversion feels automatic.

- Day 3: Drill both MPBF methods with at least eight calculations, deliberately alternating Method I and Method II so you never confuse the contribution base.

- Day 4: Memorise the Turnover Method and the CCC formula, then practise spotting negative-CCC scenarios.

- Day 5: Cover the supporting tools — EOQ, ABC, VED, JIT, factoring and the cash-management models — as quick identification flashcards.

- Day 6-7: Attempt a full timed mock, review every error, and re-drill only the formulas you missed.

Anchor this plan with active recall rather than re-reading. The fastest way to do that is to attempt our CAIIB mock tests with bilingual explanations and run quick CAIIB matching-game drills on the formulas. You will also find the full chapter notes and video classes inside the CAIIB course hub, with the paper-specific material organised under Advanced Business and Financial Management.

Common mistakes candidates make

- Confusing the MPBF contribution bases — applying 25% to the working-capital gap in Method II, or to total current assets in Method I. Read the stem first.

- Forgetting to subtract creditors in the operating cycle, which inflates the funding requirement.

- Treating CCC and operating cycle as different beasts — they share the same logic; only the framing differs.

- Memorising EOQ wrongly — the carrying cost sits in the denominator, not the numerator.

- Quoting outdated thresholds for the Turnover Method or MPBF applicability instead of confirming the current RBI position.

For the regulatory backbone that surrounds bank lending, it is worth pairing this topic with the Banking Regulation Act 1949 CAIIB BRBL guide and the credit risk measurement guide on PD, LGD, EAD and VaR. The complete set of CAIIB study guides is available on the CAIIB guides blog.

Frequently Asked Questions

Which is more conservative — MPBF Method I or Method II?

Method II is the more conservative approach because it requires a higher borrower contribution. The margin is computed as 25% of total current assets rather than 25% of the working-capital gap. As a result, larger-borrower sanctions typically use Method II, while Method I is reserved for smaller or weaker borrowers where a slightly larger bank exposure is acceptable.

What is the maximum limit under the Turnover Method?

The Nayak Committee Turnover Method was originally prescribed for aggregate working-capital limits up to a specified ceiling, which RBI has adjusted over time. Beyond that threshold, banks switch to the MPBF methods or to cash-budget-based assessment. Always verify the current operative cap against the latest RBI master direction on credit assessment before applying it.

Can a firm really have a negative cash conversion cycle?

Yes, whenever DPO exceeds the sum of DIO and DSO. This is common among large retail chains that collect cash from customers at the point of sale but pay their suppliers on extended credit of sixty to ninety days. The negative cycle means suppliers effectively finance the retailer's working capital, a powerful structural advantage.

Is EOQ actually used in real branch lending decisions?

For the exam, treat EOQ as a formula to be applied precisely. In real branch practice it is a theoretical benchmark rather than a hard rule, because actual ordering also depends on supplier reliability, transport lead time, demand variability and bulk discounts. The IIBF paper tests EOQ as a calculation; the branch tests it as judgement.

How many marks does working capital management carry in ABFM Module B?

While the exact weight varies with each paper, working capital and the surrounding credit-assessment content form one of the most heavily weighted areas of Module B. You can reasonably expect numerical questions on the operating cycle or MPBF in almost every sitting. Confirm the latest module weightage on the official IIBF syllabus before you finalise your revision priorities.

Where can I practise CAIIB ABFM working capital numericals for free?

Learning Sessions offers free, timed CAIIB mock tests with bilingual explanations, along with chapter PDFs and video classes for every ABFM module. Pairing one full mock with focused formula drills is the most efficient way to confirm readiness. Scoring around 65% or higher on your first attempt at the Module B questions is a strong sign you are on track.

Final word

Working capital management is the chapter where ABFM theory meets the daily reality of your branch. Get the operating cycle, the two MPBF methods, the Turnover Method and the supporting tools firmly in place, and you will have secured a substantial block of the ABFM paper while sharpening the credit instincts that make you better at the job itself.

Open a free CAIIB ABFM mock tonight, attempt fifteen Module B questions, and let your score guide where you revise next. For the official position on any threshold or framework mentioned here, always cross-check the source at the Indian Institute of Banking and Finance.

Related Guides

📚 Free Learning Sessions resources — connect & crack your exam

- 📝 Free mock tests — chapter-wise, exam-pattern, with instant solutions

- 🎮 Matching games — gamified revision of key terms & concepts

- 📄 Study notes & PDFs — downloadable chapter material

- 🎥 Video classes on YouTube — subscribe to @learningsessions

💬 Want the full course? WhatsApp your course name to 8360944207 and our team will set you up.

📱 Study on the go — get our iOS & Android app at iibf.store/app.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.