Atal Pension Yojana: How ₹7 a Day Builds a Guaranteed Pension

Somebody on YouTube tells you that ₹7 a day can turn into ₹25 lakh, guaranteed by the Government of India — and your first instinct is to scroll past, because that is exactly what a scam sounds like. Except this one is real. The scheme behind the claim is the Atal Pension Yojana (APY), it has been running since 2015, and the maths mostly checks out — once you understand what is actually guaranteed, and what is not.

Here is the 60-second version from our Learning Sessions channel. The full breakdown — the real contribution chart, the fine print banks will not always volunteer, and why JAIIB aspirants should know this scheme cold — follows right after.

APY in 60 seconds — the ₹7-a-day government pension (Learning Sessions) · Watch on YouTube

So what exactly is the Atal Pension Yojana?

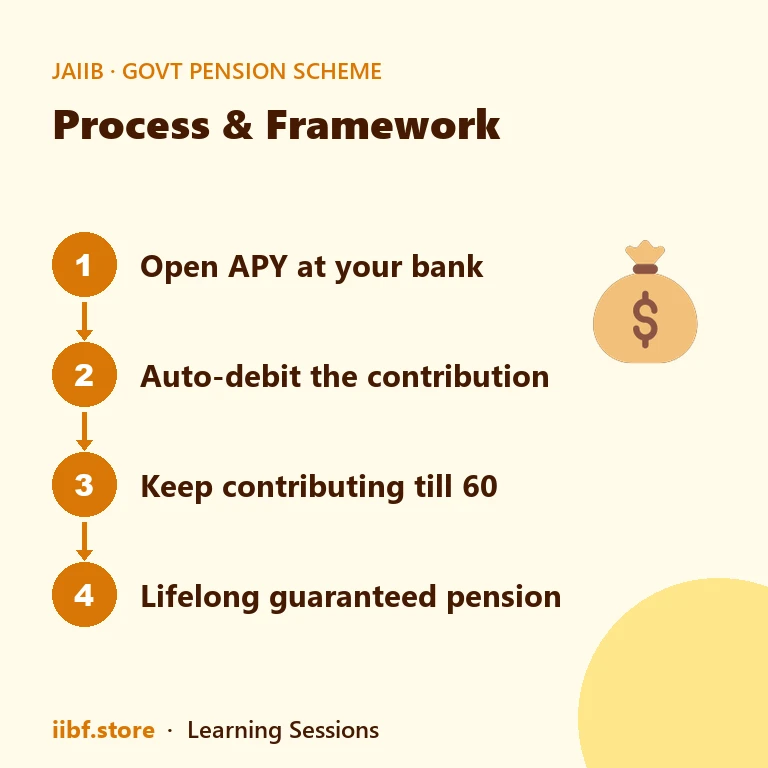

The Atal Pension Yojana is a government-backed pension scheme launched in June 2015 and administered by the Pension Fund Regulatory and Development Authority (PFRDA). It was designed for workers in the unorganised sector — people with no EPF, no NPS employer contribution, and no retirement safety net at all — though for years it was open to almost any Indian adult with a savings account.

You pick a guaranteed monthly pension slab of ₹1,000, ₹2,000, ₹3,000, ₹4,000 or ₹5,000. You contribute a fixed amount every month until you turn 60. From 60 onwards, that pension is paid to you for life. After you, your spouse receives the same pension for their lifetime. And after both of you, your nominee receives the accumulated corpus — up to ₹8.5 lakh on the top slab.

The word guaranteed is doing real work here. If the pension fund earns less than what is needed to pay your slab, the Government of India makes good the shortfall. That is written into the scheme, per the official details on jansuraksha.gov.in.

The ₹7-a-day maths — and where "₹25 lakh" comes from

The viral number comes from the youngest entry age. Join at 18 and the ₹5,000 pension slab costs just ₹210 a month — that is your ₹7 a day, roughly the price of one cutting chai. The catch, of course, is time: you will contribute for 42 years before the pension starts. Here is the official contribution chart at a glance:

| Entry age | ₹1,000 pension | ₹3,000 pension | ₹5,000 pension |

|---|---|---|---|

| 18 years | ₹42 / month | ₹126 / month | ₹210 / month |

| 25 years | ₹76 / month | ₹226 / month | ₹376 / month |

| 30 years | ₹116 / month | ₹347 / month | ₹577 / month |

| 35 years | ₹181 / month | ₹543 / month | ₹902 / month |

| 40 years | ₹291 / month | ₹873 / month | ₹1,454 / month |

| Corpus to nominee | ₹1.7 lakh | ₹5.1 lakh | ₹8.5 lakh |

Now the honest version of the ₹25 lakh claim. It is not a lump sum, and nobody hands you a cheque. It is the lifetime value of the top slab: draw ₹5,000 a month from 60 to 85 and you have received ₹15 lakh. If your spouse outlives you, the pension continues for their lifetime too. Add the ₹8.5 lakh corpus that goes to your nominee at the end, and the household comfortably crosses ₹23–25 lakh in total benefit. So the headline is fair as a lifetime figure — just know that it arrives as a monthly pension plus a legacy corpus, not as a jackpot.

The fine print that actually matters

Every scheme has clauses that decide whether it works for you. These are the ones worth reading twice:

- Entry window is 18 to 40. Not a day later. The earlier you join, the absurdly cheaper it gets — the 18-year-old pays ₹210 for the same pension that costs a 40-year-old ₹1,454.

- Income-tax payers cannot join anymore. Since 1 October 2022, anyone who is or has been an income-tax payer is barred from enrolling. Existing accounts opened before that date continue untouched.

- Contributions are auto-debited. Keep the savings account funded. Miss a debit and a penalty of ₹1 per month applies for every ₹100 of contribution due — small, but long gaps can get the account frozen, so regularise quickly.

- Exit before 60 is deliberately unattractive. Voluntary exit returns only your own contributions plus the interest they earned. The genuine exceptions are death or terminal illness.

- Death before 60: your spouse can either continue the account and take the full pension at 60, or close it and take the corpus. Death after 60: spouse draws the same pension for life; the nominee gets the corpus after both.

- You can change your slab. Upgrade or downgrade the pension amount once per financial year as your income changes.

Why bankers and JAIIB aspirants should know APY cold

If you work in a branch, APY is not trivia — it is a counter conversation you will have hundreds of times, usually with the customers who need it most and understand it least. Being able to say "for you, at 25, it is ₹376 a month for a ₹5,000 lifelong pension" from memory is the difference between a form filled and a customer walked away.

And if you are preparing for banking exams, the Atal Pension Yojana sits squarely in the JAIIB syllabus — it appears in Retail Banking & Wealth Management and in Principles & Practices of Banking, usually as a straight fact question: entry age, slab amounts, the ₹210-at-18 figure, or the nominee corpus. The government-scheme family (APY, PMJJBY, PMSBY) is one of the most reliable one-mark clusters in the paper. Drill them with our free mock tests, or make the facts stick faster with a round of match-the-scheme games. Current rates and scheme numbers also live on our RBI rates page, updated as they change.

Quick answers

Can I really get ₹25 lakh from APY?

As a lifetime total, yes — a ₹5,000 monthly pension drawn for 25 years is ₹15 lakh, the spouse continuation can add years more, and the nominee receives up to ₹8.5 lakh as corpus. As a lump sum, no. APY is a pension, not a payout.

Who cannot join the Atal Pension Yojana?

Anyone below 18 or above 40, and — since 1 October 2022 — anyone who is or has been an income-tax payer. Existing accounts opened before that cut-off continue as normal.

What happens if I miss a few contributions?

A penalty of ₹1 per ₹100 of contribution accrues per month of delay, and the arrears are collected once the account has balance. Long unpaid stretches can get the account frozen, so set the auto-debit date just after your salary credit.

Is ₹5,000 a month even worth anything in 2060?

Fair question — inflation will shrink it. Treat APY as a guaranteed floor beneath your retirement, not the whole plan. For ₹7 a day, a government-backed floor is still one of the best risk-free deals available to an 18-year-old.

One video, one chai a day, one form at your bank. Few financial decisions are this cheap to get right.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.