Turnover & Collection Ratios: JAIIB AFM Formulas, Days & Solved Example

If turnover and collection ratios feel like a blur of formulas that all look the same, you are not alone — this is exactly where most JAIIB AFM candidates lose easy marks. The good news: there are really only a handful of formulas here, they follow one logic, and once that clicks you can solve any turnover-ratio question in the paper in under a minute. This five-minute revision video makes the logic stick; the written breakdown below turns it into exam marks.

Turnover & Collection Ratios in 5 minutes · Watch on YouTube

What turnover and collection ratios actually measure

Strip away the jargon and every one of these ratios is answering a single question: how fast is money moving through the business? A turnover ratio counts how many times an item is "used up and replaced" in a year — how many times inventory sells out and restocks, how many times the debtor book is collected and rebuilt. A collection ratio takes that same idea and expresses it in days instead of times, because "we collect our dues every 45 days" is easier to act on than "our debtors turnover is 8.1 times".

That is the whole mental model. Turnover ratios are counted in times; collection and holding ratios are counted in days; and days are just 365 divided by the turnover. Hold on to that and the formulas stop being things to memorise and start being things you can rebuild from scratch.

The turnover ratios you must know cold

Three turnover ratios show up again and again in the AFM paper. Here they are with the exact formulas and what each one is really telling you.

1. Inventory (Stock) Turnover Ratio

Formula: Cost of Goods Sold ÷ Average Inventory. It tells you how many times the business sold and replaced its entire stock during the year. A higher number usually means brisk sales and lean stock; a very low number can signal slow-moving or obsolete inventory clogging up working capital. A common exam trap: the question gives you Sales, not Cost of Goods Sold. Use COGS when it is available — that is the textbook-correct numerator — and only fall back to Sales when COGS is not given.

2. Debtors (Receivables) Turnover Ratio

Formula: Net Credit Sales ÷ Average Debtors (Accounts Receivable). This counts how many times the business collected its entire receivables book in the year. The keyword is credit sales — cash sales never create a debtor, so if the question splits sales into cash and credit, use only the credit portion. If it just says "sales" with no split, treat total sales as credit sales and note your assumption.

3. Creditors (Payables) Turnover Ratio

Formula: Net Credit Purchases ÷ Average Creditors (Accounts Payable). The mirror image of the debtors ratio — it counts how many times the firm paid off its suppliers during the year. Read alongside the debtors ratio, it tells a story: a business that collects from customers faster than it pays suppliers is financing itself comfortably on supplier credit.

Turning ratios into days: the collection ratios

Every turnover ratio has a "days" twin, and this is where collection ratios live. The conversion is always the same — 365 ÷ turnover ratio (some textbooks and older IIBF questions use 360; use whichever the question specifies, and 365 by default).

- Debtors Collection Period (Average Collection Period) = 365 ÷ Debtors Turnover Ratio. The average number of days the business waits to get paid after a credit sale. Lower is healthier.

- Creditors Payment Period = 365 ÷ Creditors Turnover Ratio. The average number of days the firm takes to pay its own suppliers.

- Inventory Holding Period = 365 ÷ Inventory Turnover Ratio. The average number of days a unit of stock sits in the warehouse before it sells.

String these three together and you have drawn the operating cycle: inventory holding period plus debtors collection period gives the gross operating cycle, and subtracting the creditors payment period gives the net operating cycle (the cash conversion cycle). AFM examiners love to walk you through exactly this chain, so knowing how the pieces connect is worth far more than memorising any single formula.

A worked example — the way the exam asks it

Numbers make this concrete. Suppose a firm reports: Credit Sales ₹36,00,000; Opening Debtors ₹3,00,000; Closing Debtors ₹5,00,000.

- Average Debtors = (3,00,000 + 5,00,000) ÷ 2 = ₹4,00,000

- Debtors Turnover Ratio = 36,00,000 ÷ 4,00,000 = 9 times

- Average Collection Period = 365 ÷ 9 ≈ 41 days

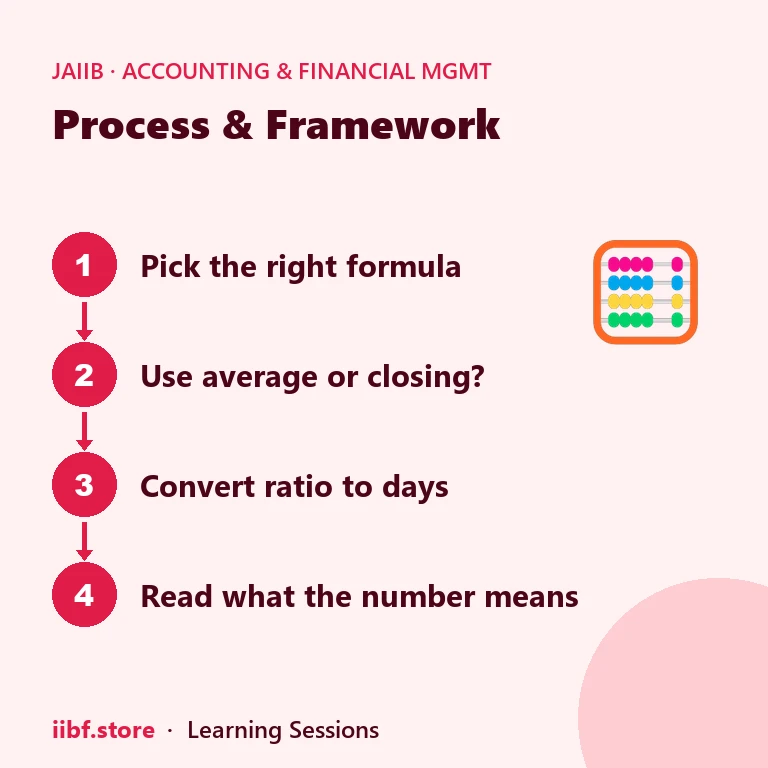

So this business collects its dues roughly every 41 days. If its credit terms to customers are "net 30", that 41-day reality flags a collection problem worth investigating. Notice the whole solution took three short steps — find the average, divide to get the turnover, divide 365 by that for the days. That three-step rhythm solves almost every turnover-and-collection question in the paper.

The mistakes that cost marks

Even candidates who know the formulas leak marks on turnover and collection ratios by slipping on the details below. Read them once and they stop happening.

- Average vs closing figures. The formulas use average debtors, creditors and inventory (opening + closing, halved). If the question only gives a closing figure, use that and say so — but never default to closing when both are provided.

- Sales vs COGS in the stock ratio. Prefer Cost of Goods Sold as the numerator for inventory turnover; use Sales only when COGS is not supplied.

- Cash vs credit. Debtors and creditors ratios use credit sales and credit purchases — strip out the cash portion when the split is given.

- 360 vs 365 days. Both appear in IIBF material. Follow the question's instruction; default to 365 when it is silent.

How to lock this in before exam day

Turnover and collection ratios reward drilling, not re-reading. Watch the five-minute revision once for the logic, then solve ten mixed problems until the three-step rhythm is automatic. You will find these ratios sitting inside the broader ratio-analysis chapter of the JAIIB AFM syllabus, alongside liquidity and profitability ratios — and they combine beautifully with those in case-study questions.

Put them to work with our JAIIB mock tests, which mirror the exact numeric style shown above, and use the match-the-formula game to make sure you never again mix up the debtors ratio with the creditors ratio under time pressure. If you would rather revise the whole ratio family in one sitting, the concept classes on our JAIIB blog cover liquidity, solvency and profitability ratios with the same worked-example approach.

Quick answers

What is the difference between a turnover ratio and a collection ratio?

A turnover ratio is measured in times (how many times an item cycles in a year); a collection or holding ratio expresses the same thing in days, calculated as 365 divided by the turnover ratio.

Should I use sales or cost of goods sold for inventory turnover?

Use Cost of Goods Sold when it is given — that is the textbook-correct numerator. Use Sales only as a fallback when COGS is not provided in the question.

Do I use 360 or 365 days for the collection period?

Both appear in IIBF questions. Always follow the number specified in the question; when it is silent, use 365.

Why does a high debtors collection period matter?

It means cash is stuck with customers for longer, straining working capital. If the collection period is well above the credit terms the firm offers, it signals weak collection or lax credit control.

Turnover and collection ratios are among the most predictable marks in the AFM paper once this logic is in place. Five minutes of video, one three-step rhythm, and a topic that used to eat time now hands you easy marks. That is the trade every AFM revision should make.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.