FATF Mutual Evaluation of India: KYC-AML Exam Guide (2026)

Every few years, a country's entire anti-money laundering machinery gets graded by outside examiners — and the FATF mutual evaluation of India, whose report was adopted in 2024, is one of the most important scorecards in the KYC-AML syllabus. For bank officers and IIBF candidates, understanding how this assessment works explains why RBI keeps tightening KYC circulars and why "compliance" is never a one-time checkbox.

🔍 What Is a FATF Mutual Evaluation?

The Financial Action Task Force (FATF) is the global standard-setter for anti-money laundering and counter-terrorist financing (AML/CFT) policy. Every member jurisdiction is periodically subjected to a "mutual evaluation" — a peer-review exercise where assessors from other member countries and FATF-Style Regional Bodies (FSRBs) examine how well a nation's laws, institutions, and supervisors actually work in practice. For India, this exercise was carried out by the Asia/Pacific Group on Money Laundering (APG), a FATF-affiliated FSRB, with an on-site visit in November 2023. The assessors met RBI, SEBI, FIU-IND, IRDAI, enforcement agencies, and banks directly, testing whether AML/CFT rules translate into real-world outcomes and not just paperwork. This is fundamentally different from a self-assessment: evaluators independently verify records, interview supervisors, and stress-test whether suspicious transactions actually get detected, reported, and acted upon. The framework used for this exercise draws on the same international guidelines & standards that shape every jurisdiction's AML architecture, which is why the topic sits at the intersection of global policy and domestic banking practice. Candidates should note that mutual evaluations are not punitive audits by default — they are diagnostic tools meant to identify gaps before they become systemic vulnerabilities exploited by launderers or terror financiers.

💡 Exam Tip: Remember the sequence — on-site visit → draft Mutual Evaluation Report (MER) → FATF Plenary discussion → adoption → publication. Questions often test which stage a specific activity belongs to.

🇮🇳 How India's 2024 Mutual Evaluation Unfolded

India's third-round Mutual Evaluation Report was adopted at the FATF Plenary in June 2024 and published shortly after. The outcome placed India in the "regular follow-up" category — the highest rating band available, reserved for jurisdictions with the strongest AML/CFT frameworks. Only a small handful of G20 economies have ever achieved this category on their first attempt at a mutual evaluation of this scale, making it a genuinely significant milestone referenced widely in exam material and RBI communications. The report recognised India's progress in areas such as financial inclusion-linked KYC simplification, the reach of FIU-IND's reporting network, and coordinated action against terror financing channels. It also flagged follow-up areas, including supervision of non-banking sectors and beneficial-ownership transparency, which India is required to address in periodic follow-up reports submitted to FATF. This entire evaluation cycle sits on the legal scaffolding built through legislation at the national level — principally the Prevention of Money Laundering Act — which mutual evaluators use as the benchmark against which technical compliance is measured. For bankers, the practical takeaway is that RBI's KYC Master Direction updates are rarely arbitrary; many trace directly back to gaps or recommendations flagged during evaluation cycles like this one.

📋 Technical Compliance vs Effectiveness Ratings

A mutual evaluation report actually produces two distinct sets of scores, and exam questions frequently confuse the two. The first is "technical compliance," which rates a country against each of the FATF Recommendations on a four-point scale: Compliant (C), Largely Compliant (LC), Partially Compliant (PC), or Non-Compliant (NC). This measures whether the right laws and regulations exist on paper. The second, more demanding, measure is "effectiveness," assessed against 11 Immediate Outcomes covering areas such as supervision, financial intelligence use, investigation and prosecution, and international cooperation. Effectiveness is rated High, Substantial, Moderate, or Low, and it measures whether the legal framework actually produces real-world results — arrests, convictions, asset freezes, and disrupted networks — rather than just existing in statute. A country can score well on technical compliance while still scoring poorly on effectiveness if enforcement is weak, which is precisely why FATF introduced the effectiveness dimension in its current methodology. India's 2024 report showed strong results across both dimensions, a key reason it secured the regular follow-up category rather than the more intensive "enhanced follow-up" track that many G20 peers remain on.

⚠️ Common Mistake: Candidates often assume a high technical compliance score alone guarantees a good outcome. FATF weighs effectiveness ratings just as heavily — sometimes more — when deciding the follow-up category.

🌐 Regular Follow-Up: Why India's Rating Matters

Countries placed under "enhanced follow-up" must report back to FATF annually and face closer scrutiny, sometimes including grey-listing risk if progress stalls. "Regular follow-up," by contrast, means a country reports on a lighter three-year cycle, reflecting confidence that its AML/CFT system is fundamentally sound. This rating has tangible consequences beyond prestige: it affects how foreign banks perceive risk when assessing correspondent banking due diligence for Indian institutions, and it feeds directly into country risk and money laundering assessments that global banks run before onboarding Indian counterparties. A stronger FATF standing lowers the perceived risk premium attached to Indian financial flows — much as types of inflation in India shapes how monetary policy is priced, a country's FATF standing shapes how global capital prices sovereign and banking risk. This can ease cross-border trade finance and remittance corridors. It also validates the layered structure of India's AML/CFT institutions — RBI, SEBI, IRDAI, FIU-IND, and the Enforcement Directorate — working under a common national framework rather than siloed rulebooks. For exam purposes, understand that the follow-up category is reviewed periodically, so a good 2024 outcome does not mean India is permanently exempt from scrutiny; sustained implementation is what keeps a jurisdiction off enhanced monitoring lists.

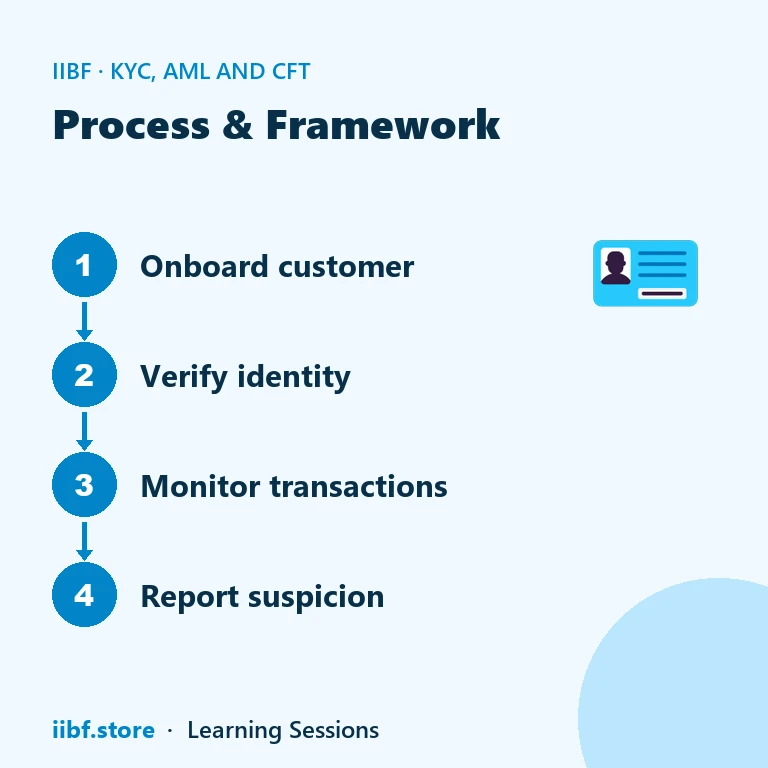

Mutual evaluation findings do not stay confined to policy circles — they flow straight into day-to-day banking compliance. When FATF or APG flags a gap, RBI typically responds with circular updates, stricter reporting timelines, or enhanced supervisory checks, all of which show up as fresh amendments to the RBI KYC Master Direction. Compliance officers should treat every mutual evaluation cycle as an early-warning signal for upcoming regulatory change, not a distant international formality. Banks are also directly assessed as part of the "effectiveness" testing — evaluators sample real transaction monitoring files, STR/CTR filing timeliness, and customer due diligence records during on-site visits. This is one reason why internal audit and RBI inspections increasingly ask branches to demonstrate, with evidence, that KYC and monitoring controls work in practice rather than existing only in policy manuals. The same effectiveness lens is why banks maintain rigorous sanctions screening in banks processes and monitor politically exposed persons closely — both are areas FATF assessors test directly through file sampling during a mutual evaluation. FATF evaluates outcomes, not just rulebooks — a bank's actual STR quality and monitoring effectiveness matter as much as having a policy document on file. The table below summarises how the ratings fit together and where India landed in 2024.

| Rating Track | Scale Used | Best Category | India 2024 Outcome | Reduces Global Risk Flag? |

|---|---|---|---|---|

| Technical Compliance | C / LC / PC / NC | Compliant (C) | Mostly C/LC across 40 Recommendations | ✅ |

| Effectiveness (11 Immediate Outcomes) | High / Substantial / Moderate / Low | High | Substantial to High on most outcomes | ✅ |

| Follow-Up Category | Regular vs Enhanced | Regular Follow-Up | Regular Follow-Up (3-year cycle) | ✅ |

| Grey List Status | Listed / Not Listed | Not Listed | Not Listed | ✅ |

| Enhanced Monitoring Track | Applies if outcomes are weak | Not Applicable | Not Applicable | ❌ (if applicable) |

🧠 Practice MCQs: FATF Mutual Evaluation of India

Q1. Which FATF-affiliated body conducted the on-site visit for India's 2023-24 mutual evaluation? (a) Egmont Group (b) Asia/Pacific Group on Money Laundering (APG) (c) Basel Committee (d) Wolfsberg Group

Answer: (b) — APG, a FATF-Style Regional Body, carried out India's on-site assessment in November 2023.

Q2. India's 2024 Mutual Evaluation Report placed the country in which follow-up category? (a) Enhanced follow-up (b) Grey list (c) Regular follow-up (d) Black list

Answer: (c) — Regular follow-up is the highest category, reserved for the strongest-performing AML/CFT frameworks.

Q3. Technical compliance ratings in a mutual evaluation are scored on which scale? (a) High/Moderate/Low (b) Compliant/Largely Compliant/Partially Compliant/Non-Compliant (c) Pass/Fail (d) A/B/C/D grades

Answer: (b) — Technical compliance uses the four-point C/LC/PC/NC scale against each of the 40 Recommendations.

Q4. The 11 Immediate Outcomes in a mutual evaluation primarily measure: (a) Bank branch profitability (b) Whether AML/CFT laws produce real-world enforcement results (c) Deposit insurance coverage (d) Foreign exchange reserves

Answer: (b) — Effectiveness ratings test whether the legal framework actually delivers outcomes like prosecutions and asset seizures, not just legislation.

Q5. What is the typical review cycle for a country placed under "regular follow-up"? (a) Annual (b) Three years (c) Ten years with no interim reporting (d) Six months

Answer: (b) — Regular follow-up jurisdictions report back to FATF on a lighter, roughly three-year cycle compared to annual reporting for enhanced follow-up.

Want chapter-wise mock tests with 100+ MCQs? Start practising free →

What is a FATF mutual evaluation of India in simple terms?

It is a peer-review exercise where international assessors examine whether India's AML/CFT laws, institutions like FIU-IND and RBI, and banks actually detect and act on money laundering and terror financing, not just have rules on paper.

When was India's most recent mutual evaluation completed?

The on-site visit took place in November 2023, and the Mutual Evaluation Report was adopted at the FATF Plenary in June 2024 and published soon after.

What follow-up category did India receive?

India was placed in the "regular follow-up" category, the highest rating band, meaning it reports back to FATF on a lighter three-year cycle rather than facing annual enhanced monitoring.

Why does the FATF mutual evaluation matter for bank employees?

Findings from mutual evaluations directly shape RBI's KYC Master Direction updates, supervisory checks, and reporting requirements, so understanding the process helps compliance staff anticipate regulatory change.

The FATF mutual evaluation of India is more than an international scorecard — it is the mechanism that keeps RBI's KYC circulars, FIU-IND reporting, and bank-level monitoring aligned with global standards. For IIBF candidates, tying this process to the underlying legislation and international guidelines makes the whole KYC-AML syllabus click into place. Reinforce the concept further via the KYC-AML blog hub, then test your recall with full-length CAIIB practice sets or start a free mock right away.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.

Keep reading