MSME Classification in India: CGTMSE, MUDRA & IIBF Guide 2026

MSME classification in India is the foundation on which every credit decision, subsidy and priority-sector benefit for a small business is built — and it is the single most-tested concept in the IIBF Certificate Course on MSME. Get the classification right and a banker can price the loan correctly, attach the appropriate guarantee cover and steer the borrower to the right government scheme. Get it wrong, and the entire proposal unravels.

This guide explains the revised criteria in plain language, then layers on the schemes examiners love — CGTMSE, MUDRA, PMEGP, Stand-Up India, priority-sector status and TReDS — with a study plan, comparison tables and a snippet-ready FAQ so you walk into the exam hall genuinely prepared.

Key Takeaways

- Since July 2020, India uses a composite criterion — investment in plant, machinery or equipment and annual turnover — with the same slabs for manufacturing and services.

- Micro: investment up to Rs 1 crore, turnover up to Rs 5 crore. Small: up to Rs 10 crore and Rs 50 crore. Medium: up to Rs 50 crore and Rs 250 crore.

- Cross the ceiling in either investment or turnover and the unit moves up a category; export turnover is excluded from the turnover limit.

- CGTMSE gives collateral-free guarantee cover to micro and small units only — medium enterprises are out of scope.

- MUDRA funds non-farm micro units in three slabs: Shishu, Kishore and Tarun.

- All bank credit to MSMEs counts as priority sector lending.

What MSME Classification in India Means Today

Before July 2020, classification depended only on investment, and manufacturing and service units were judged on different scales. That created endless disputes and discouraged firms from growing on the books. The revised framework replaced it with a single, transparent composite criterion that applies uniformly across sectors.

Under the current rules an enterprise is graded on two parameters together:

- Investment in plant and machinery or equipment, and

- Annual turnover of the enterprise.

The same three slabs now cover both a textile mill and a software consultancy. This removal of the old manufacturing-versus-services distinction is a favourite one-mark trap, so fix it firmly in memory.

The Revised MSME Classification Criteria (Micro, Small, Medium)

Here is the grid that drives direct objective questions in the MSME paper. Learn it as a 3×2 table, not as loose sentences — examiners test the exact crossover figures.

| Category | Investment (plant & machinery/equipment) | Annual turnover |

|---|---|---|

| Micro | Up to Rs 1 crore | Up to Rs 5 crore |

| Small | Up to Rs 10 crore | Up to Rs 50 crore |

| Medium | Up to Rs 50 crore | Up to Rs 250 crore |

Three rules turn this grid from memorised numbers into usable knowledge:

- Either-or, not both. If an enterprise breaches the ceiling on investment or turnover, it is pushed up to the next category. You do not need both conditions to be crossed.

- Exports are excluded. Export turnover is deliberately kept out of the turnover computation, a built-in incentive that lets exporters grow without losing MSME benefits.

- Udyam does the validating. Registration is online through the Udyam Registration portal, which is linked to PAN and GST and self-validates the figures, so the classification is largely automated.

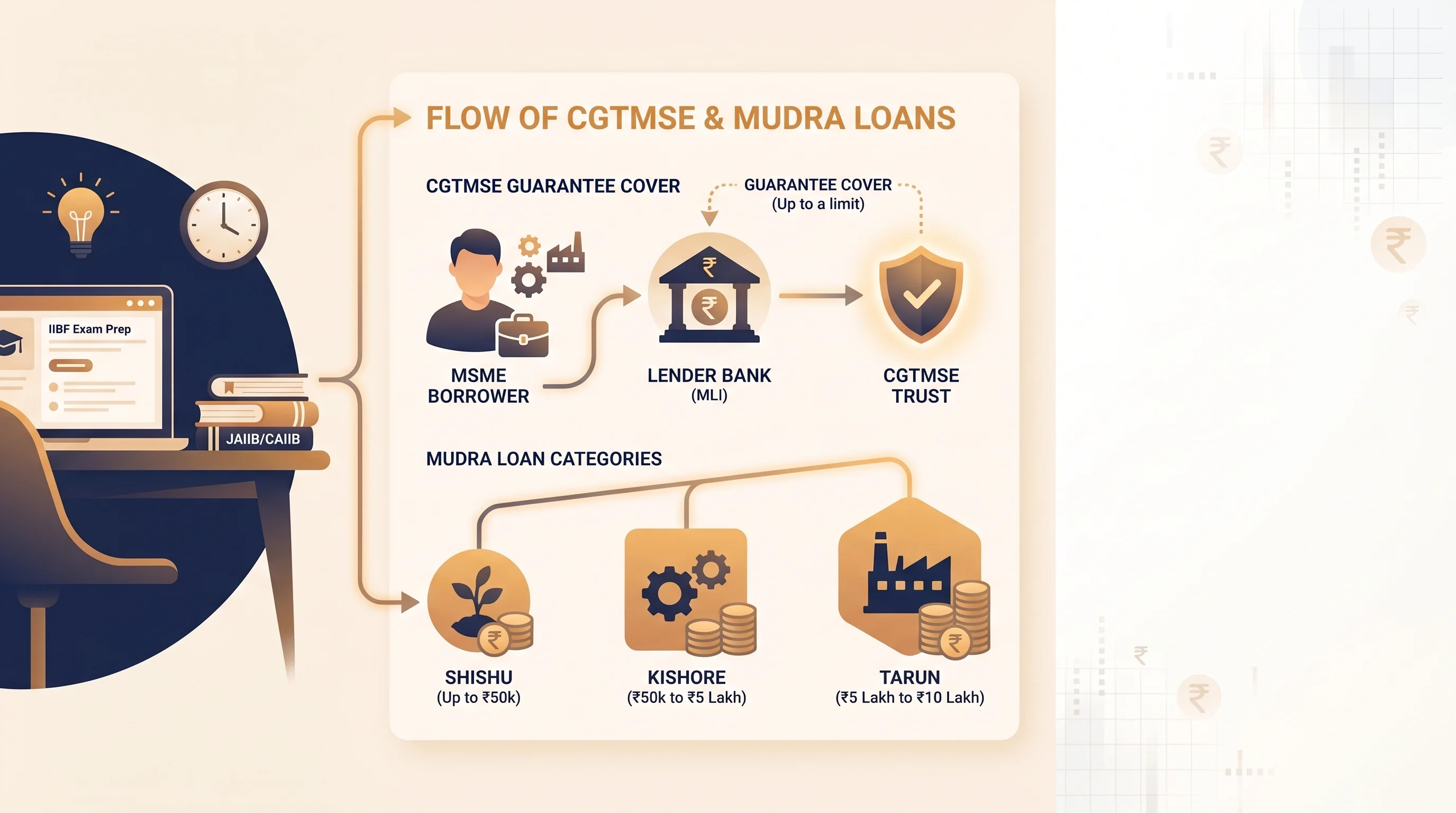

CGTMSE: Collateral-Free Credit Guarantee

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) lets banks lend to micro and small units without collateral or a third-party guarantee. Set up by the Government of India and SIDBI, the trust provides guarantee cover on the credit facility, so the lender’s downside risk is sharply reduced and genuine first-generation entrepreneurs become bankable.

Key features that map directly to exam questions:

- Eligibility: micro and small enterprises only — medium enterprises are outside CGTMSE’s scope. This is exactly why accurate classification matters before you even touch the scheme.

- Cover ceiling: available on loans up to a notified limit that has been progressively raised — as per the latest CGTMSE notification, currently up to Rs 5 crore per borrower (always confirm the prevailing ceiling on the official notification).

- Higher cover is extended to micro units, women entrepreneurs and enterprises in specified regions.

- Guarantee fee: banks pay an annual, risk-based fee for the cover.

Linking the right scheme to the right category is the whole point of classification. A medium enterprise simply cannot be parked under CGTMSE — recognise that in a case stem and you save an easy mark. Reinforce each scheme’s eligibility with our MSME schemes matching game, and read the focused explainer on the CGTMSE guarantee scheme — when banks use it instead of MUDRA.

MUDRA, PMEGP and the Wider Funding Ecosystem

Around the classification sit a cluster of refinance and subsidy schemes that examiners ask you to match to a borrower profile.

The Pradhan Mantri MUDRA Yojana finances non-farm, income-generating micro units through three named slabs — Shishu, Kishore and Tarun — with an enhanced Tarun-plus slab for disciplined repeat borrowers. MUDRA loans are refinanced by the MUDRA institution and are also covered under a dedicated credit guarantee, which keeps them collateral-free.

| MUDRA category | Loan amount | Typical borrower |

|---|---|---|

| Shishu | Up to Rs 50,000 | First-time, very small ventures |

| Kishore | Rs 50,000 to Rs 5 lakh | Growing units needing working capital |

| Tarun | Rs 5 lakh to Rs 10 lakh | Established micro enterprises scaling up |

The Prime Minister’s Employment Generation Programme (PMEGP), run by KVIC, provides a margin-money subsidy on bank loans for new micro enterprises, with higher subsidy rates for special categories and rural areas. The Stand-Up India scheme funds greenfield enterprises promoted by SC/ST and women entrepreneurs. For the paper, practise matching a borrower’s profile — new versus existing, social category, urban versus rural — to MUDRA, PMEGP or Stand-Up India. Our deep-dive on the MUDRA loan scheme — Shishu, Kishore, Tarun works through these distinctions, while the Stand-Up India scheme for SC/ST and women entrepreneurs covers eligibility in detail.

Priority Sector Status, Restructuring and TReDS

All bank credit to MSMEs qualifies as priority sector lending, which is precisely why banks chase this segment to meet their regulatory targets. The Reserve Bank of India has also issued specific norms for the restructuring of MSME advances and a framework for the revival and rehabilitation of stressed micro and small units — including a committee mechanism and a time-bound corrective action plan.

Two more pillars round out the ecosystem:

- TReDS (Trade Receivables Discounting System): an electronic platform that lets MSMEs convert receivables from large buyers into immediate cash, easing the chronic problem of delayed payments.

- The 45-day rule: the MSMED Act mandates payment to MSME suppliers within 45 days and provides for compound interest on delayed payments at three times the RBI bank rate.

When a unit slips into stress, recovery routes such as SARFAESI, one-time settlement and Lok Adalat come into play — our guide to NPA recovery in MSME lending walks through each. Tying classification, guarantee schemes, priority-sector status and the receivables ecosystem together gives you full command of this paper. Anchor it all from the Certificate Course on MSME hub and the Small and Medium Enterprises in India module.

How to Study MSME Classification: A 7-Day Plan

Definitions alone do not pass this paper — application does. Use this compact sequence in your final week:

- Day 1–2: Burn the classification grid into memory. Write the 3×2 table from blank five times and test the either-or rule with mini-scenarios.

- Day 3: Layer CGTMSE — who is eligible, the cover ceiling, why medium units are excluded.

- Day 4: Master MUDRA slabs, PMEGP and Stand-Up India by matching borrower profiles.

- Day 5: Add priority-sector status, restructuring norms, TReDS and the 45-day payment rule.

- Day 6: Attempt a full-length timed MSME mock test and review every wrong answer.

- Day 7: Revisit only your weak spots and skim the latest IIBF notification for any scheme tweaks.

Common Mistakes to Avoid

- Memorising figures but not the either-or rule. Crossing one ceiling is enough to move a unit up — many candidates wrongly assume both must be breached.

- Putting a medium enterprise under CGTMSE. The guarantee covers micro and small only.

- Including export turnover in the turnover limit. It is excluded.

- Confusing MUDRA, PMEGP and Stand-Up India. Keep a running list of easily-mixed schemes and test the distinctions until they are automatic.

- Mishandling negatively-phrased stems such as “which is NOT”. Read each question twice; these trip up even well-prepared candidates.

Frequently Asked Questions

What are the revised MSME classification limits in India?

Micro means investment up to Rs 1 crore and turnover up to Rs 5 crore. Small means up to Rs 10 crore and Rs 50 crore. Medium means up to Rs 50 crore and Rs 250 crore. The same limits apply to both manufacturing and service enterprises.

Does an enterprise need to cross both investment and turnover limits to be reclassified?

No. Breaching the ceiling on either investment or turnover is enough to move the unit to the next category. Both conditions do not have to be crossed at once, which is a frequent exam trap.

Does CGTMSE cover medium enterprises?

No. CGTMSE provides collateral-free guarantee cover only to micro and small enterprises. Medium enterprises fall outside its scope, which is exactly why correct classification must come first.

What are the three MUDRA loan categories?

They are Shishu (up to Rs 50,000), Kishore (Rs 50,000 to Rs 5 lakh) and Tarun (Rs 5 lakh to Rs 10 lakh). A Tarun-plus slab exists for eligible repeat borrowers, and all categories target non-farm, income-generating micro units.

Within how many days must MSME suppliers be paid?

The MSMED Act mandates payment to MSME suppliers within 45 days. If the buyer fails to pay in time, it becomes liable to pay compound interest at three times the RBI bank rate on the outstanding amount.

Is all bank credit to MSMEs treated as priority sector lending?

Yes. Credit extended to MSMEs qualifies as priority sector lending, which is why banks actively pursue this segment to meet regulatory targets. You should also know the RBI’s restructuring and revival framework for stressed micro and small units. You can verify current norms on the official IIBF website.

Conclusion

Nail the three-slab MSME classification grid first, then layer CGTMSE, MUDRA, PMEGP, Stand-Up India, priority-sector status and TReDS on top. That sequence mirrors how a real banker assesses an MSME proposal — and exactly how the IIBF examiner frames questions. Master it, practise under timed conditions, and this paper becomes one of your strongest. Explore every guide for this exam on our MSME study blog and start your next timed mock today.

Related Guides

📚 Free Learning Sessions resources — connect & crack your exam

- 📝 Free mock tests — chapter-wise, exam-pattern, with instant solutions

- 🎮 Matching games — gamified revision of key terms & concepts

- 📄 Study notes & PDFs — downloadable chapter material

- 🎥 Video classes on YouTube — subscribe to @learningsessions

💬 Want the full course? WhatsApp your course name to 8360944207 and our team will set you up.

📱 Study on the go — get our iOS & Android app at iibf.store/app.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.