MSME Classification Revised: Micro, Small & Medium Thresholds

MSME classification is the single rule that decides whether a borrower in your branch is a Micro, Small or Medium enterprise — and that one label quietly drives priority-sector reporting, scheme eligibility, and the concessional pricing you offer. Yet ask three loan officers what officially makes a firm "Small" and you will often get three different answers. This guide settles it in plain, working-banker language, then shows exactly how the topic appears in the IIBF Certificate Course on MSME.

The framework was overhauled in mid-2020 alongside the amendments to the MSMED Act, and the Ministry has continued to refine the operative limits since. The big change was a move to a composite, dual-criterion definition built on two numbers — investment and turnover — applied uniformly to both manufacturing and service enterprises. Below, we unpack the thresholds, the Udyam Registration that makes a classification official, the priority-sector consequences, and the mistakes that quietly create regulatory exposure.

Key takeaways

- MSME classification uses a composite rule: investment in plant & machinery / equipment AND annual turnover — both limits must be met.

- The same thresholds apply to manufacturing and services, a major simplification from the pre-2020 structure.

- Udyam Registration is the free, online, self-declaration mechanism that makes the classification official and PSL-eligible.

- Loans to Micro and Small enterprises automatically qualify as priority-sector lending; Medium qualifies subject to conditions.

- Always confirm the current figures against the latest released MSME Ministry gazette notification or RBI master direction before sanction.

Why MSME classification matters at the branch level

Classification is not a clerical formality — it changes the economics of a loan file. Three branch realities depend on getting it right.

Priority-sector lending (PSL). Credit to Micro and Small enterprises counts as PSL automatically, and Medium-enterprise credit counts subject to specified conditions. Misclassify a borrower and you misreport PSL — a direct regulatory exposure that surfaces in audit and inspection.

Scheme eligibility. CGTMSE, MUDRA, PMEGP, Stand-Up India and the Credit Linked Capital Subsidy Scheme each carry tier-specific eligibility. A wrongly classified borrower gets slotted into the wrong scheme — or fails to get sanctioned at all.

Pricing and concessions. Most bank product masters offer concessional rates and processing-fee waivers to Micro and Small enterprises. Misclassification means either overcharging a genuine Micro unit or quietly underpricing a Medium one.

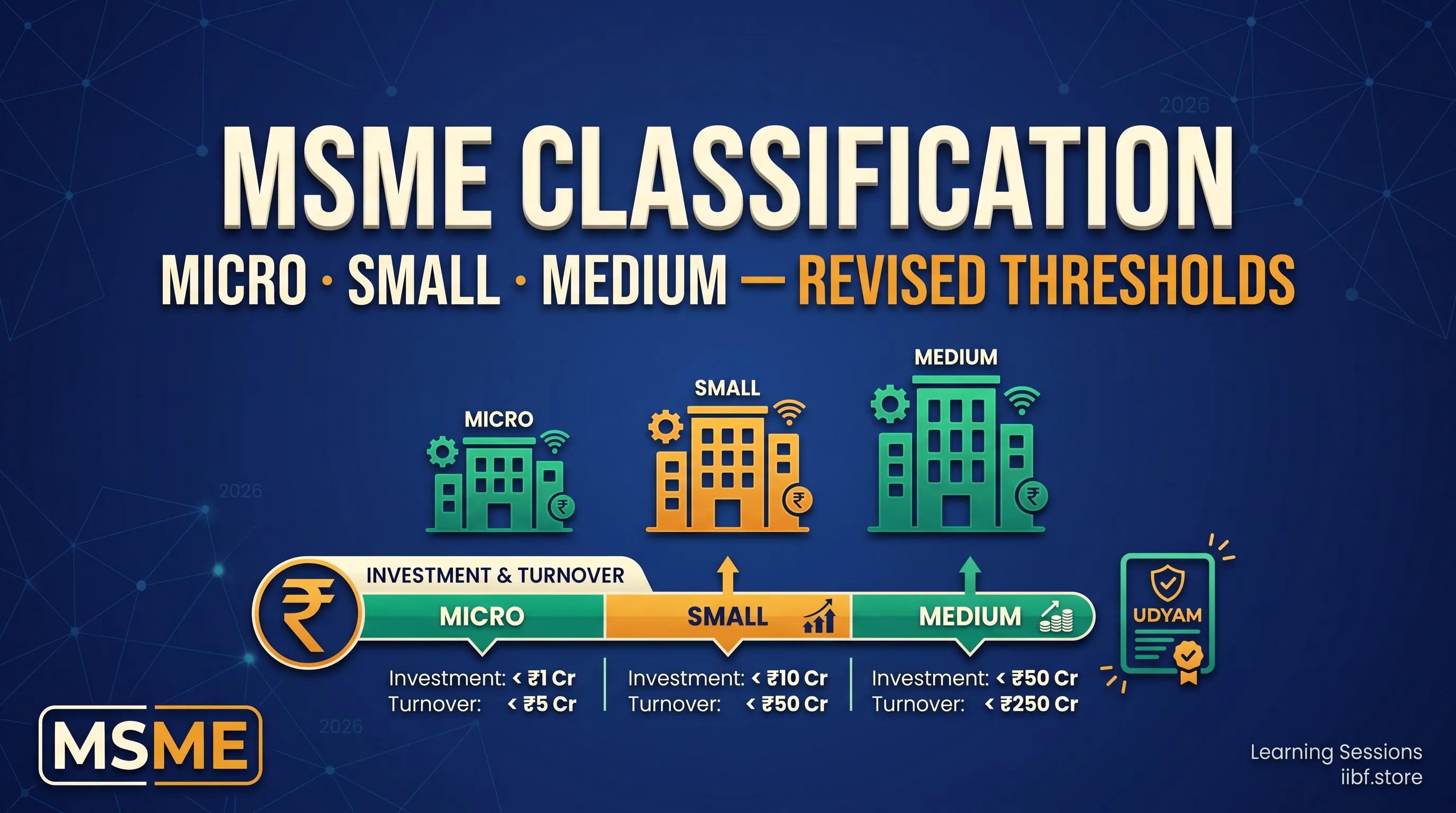

The revised thresholds — a dual investment-and-turnover criterion

Since the 2020 revision, MSME classification rests on two criteria applied together: investment in plant and machinery or equipment, and annual turnover. The connector is AND, not OR. An enterprise must satisfy both limits of a tier to sit in that tier; breach either one and it moves up.

Crucially, the limits are now identical for manufacturing and service enterprises — the old separate-criteria split is gone. As per the framework introduced in the 2020 revision, the indicative limits are:

| Tier | Investment in plant & machinery / equipment | Annual turnover |

|---|---|---|

| Micro | Up to ₹1 crore | Up to ₹5 crore |

| Small | Up to ₹10 crore | Up to ₹50 crore |

| Medium | Up to ₹50 crore | Up to ₹250 crore |

A worked example you can reuse at the desk

Numbers make the dual rule stick. Take an auto-component manufacturer with ₹8 crore invested in plant and machinery and an annual turnover of ₹40 crore.

- Investment ≤ ₹10 crore → qualifies for Small.

- Turnover ≤ ₹50 crore → qualifies for Small.

- Both limits met → classification is Small Enterprise.

Now suppose turnover grows to ₹60 crore next financial year while investment stays at ₹8 crore. Investment still says Small, but turnover has crossed the ₹50 crore Small ceiling. Because either breach pushes the firm up, the unit is reclassified as a Medium Enterprise — and its scheme and PSL treatment shift accordingly. This is precisely why a once-a-year refresh at renewal is non-negotiable.

Udyam Registration — the official mechanism

A classification only becomes operative once it is captured on Udyam Registration, the Government of India portal that replaced the older Udyog Aadhaar Memorandum (UAM) system. Its design removes most of the friction that plagued the old regime.

- Free of cost and fully online, paperless, based on self-declaration.

- Auto-fetches PAN, GSTIN and ITR data from the CBDT and GST systems to derive investment and turnover — the figures are not left to the applicant's say-so.

- Issues a unique Udyam Registration Number (URN) and an Udyam Certificate.

- A single registration covers the whole enterprise nationwide, including all plants and branches.

- Reclassification is automatic when ITR/GST data shows a threshold has been crossed — neither the bank nor the borrower files a fresh application.

The branch discipline is simple: insist on the Udyam Registration Certificate in every MSME loan file. Without it you cannot claim PSL classification, and you cannot enrol the loan under any MSME credit-guarantee or subsidy scheme. For the full course syllabus around this, see the Certificate Course on MSME hub and the dedicated module on small and medium enterprises in India.

Priority Sector Lending implications

RBI requires Scheduled Commercial Banks to lend a minimum share of their Adjusted Net Bank Credit (ANBC) — or the Credit Equivalent of Off-Balance-Sheet Exposure, whichever is higher — to priority sectors. The headline PSL target is 40% of ANBC for domestic banks (subject to the current RBI master direction), and MSME is one of the recognised priority sectors.

Within MSME there are sub-targets — for example, a sub-target for Micro enterprises of 7.5% of ANBC as per the operative PSL master direction. These percentages and definitions are revised by RBI from time to time, so always read them against the latest released master direction rather than from memory.

The stakes are financial, not just procedural. A shortfall against PSL targets must be parked with NABARD, SIDBI and similar institutions under funds such as the Rural Infrastructure Development Fund (RIDF) and MSME refinance windows. Those deposits earn a sub-market return, so a PSL shortfall is a direct drag on profitability — which is exactly why accurate classification at the file level matters to the whole bank.

Trader inclusion — the recent expansion

Until July 2021, traders sat outside the MSME definition. The MSME Ministry then notified that retail and wholesale trade activities are eligible for MSME (Udyam) registration, with PSL classification subject to specified conditions and turnover-based criteria. This widened the eligible MSME population substantially and brought a large class of trading borrowers into scheme coverage. Because the precise scope has evolved, confirm the latest position from the operative MSME Ministry gazette notification before sanctioning trade-only enterprises.

A practical desk routine for getting classification right

Turn the rules into a repeatable checklist you can run on any MSME file, whether at first sanction or at annual renewal.

- Pull the Udyam Certificate first. No certificate, no PSL tag, no scheme — make it the first document you request.

- Read both numbers. Note investment in plant & machinery/equipment and annual turnover, and confirm both sit inside the same tier.

- Cross-check against the latest notification. Reconcile the limits with the current MSME Ministry / RBI release before you finalise the tier.

- Exclude export turnover where applicable when testing the turnover limit (see the FAQ below).

- Tag PSL and scheme eligibility consistently in the system once the tier is fixed.

- Diarise an annual refresh. Re-verify the tier at every renewal so a firm that has grown into Medium — or shrunk back to Small — is reclassified promptly.

Common branch-side classification mistakes

- Using only one criterion. Checking investment but ignoring turnover (or vice versa). Both must be satisfied — it is an AND test.

- Never refreshing the tier. A unit classified Small in year one may be Medium by year three. Re-verify at renewal.

- Treating Udyam as optional. Without it the loan cannot be PSL-classified or enrolled in any MSME scheme.

- Applying legacy numbers. The pre-2020 structure had separate manufacturing/service criteria — do not carry old thresholds into the new composite rule.

- Ignoring downward reclassification. When turnover falls and a firm moves back from Medium to Small, Micro/Small scheme eligibility reactivates — update the customer master and bureau records.

MSME classification in the IIBF MSME exam

For candidates of the Certificate Course on MSME, this is a high-yield topic that reliably contributes several marks per paper. The questions tend to be precise and figure-based, so the limits and the Udyam mechanism are worth memorising cold. Typical framings include:

- The investment limit for a Micro Enterprise (up to ₹1 crore).

- The turnover limit for a Small Enterprise (up to ₹50 crore).

- The authority that issues Udyam Registration (the MSME Ministry, via the Udyam portal).

- Whether manufacturing and service criteria are the same or different (the same, since the 2020 revision).

- The Priority Sector sub-target for Micro Enterprises (as per the current PSL master direction).

Drill these on chapter-wise MSME mock tests and reinforce recall with quick matching-game drills. For wider context, our MSME credit schemes explainer and the MSME credit-assessment field guide connect classification to the lending decisions that follow, and you can browse every MSME guide in one place.

Frequently Asked Questions

What exactly is the revised MSME classification?

It is a composite definition based on two limits applied together: investment in plant and machinery or equipment, and annual turnover. An enterprise must satisfy both limits of a tier to be classified Micro, Small or Medium. The same thresholds apply to manufacturing and service enterprises following the 2020 revision.

Is the classification based on investment or turnover?

Both. The rule is a dual, AND-based criterion, so investment and turnover must each fall within the same tier. If a firm breaches either limit, it moves up to the next tier. This is the single most common point candidates and loan officers get wrong.

If a firm's turnover crosses ₹250 crore, does it still get MSME benefits?

No. Once investment exceeds ₹50 crore or turnover exceeds ₹250 crore, the enterprise moves beyond the Medium tier and ceases to be an MSME. PSL classification stops and MSME scheme eligibility ends from that point.

Are exports counted in turnover for MSME classification?

As per the current MSME Ministry notification, export turnover is excluded from the turnover criterion for classification purposes. The carve-out exists so that growing exports do not prematurely push an enterprise into a higher tier. Always confirm the current treatment against the latest released notification.

Does an MSME need a fresh Udyam Registration every year?

No. Udyam Registration is a one-time process and the certificate does not expire. Reclassification between tiers happens automatically based on the latest ITR and GSTIN data linked to the PAN, so no annual re-application is required.

Can a new firm register as an MSME before it has employees?

Yes. Udyam Registration is driven by investment and turnover, not headcount, so a new enterprise with planned investment can register and begin availing benefits as it becomes operational. The system simply tracks the financial figures over time.

Final word

MSME classification looks deceptively simple — two numbers, three tiers — but its power lives in the discipline around it: the AND rule, the Udyam certificate in every file, and the annual refresh that keeps each borrower on the correct PSL line. Master those three habits and your MSME portfolio stays clean, your scheme tagging stays accurate, and your exam answers stay sharp. Confirm the live figures against the official notification, practise the recall, and the rest follows naturally.

Related Guides

📚 Free Learning Sessions resources — connect & crack your exam

- 📝 Free mock tests — chapter-wise, exam-pattern, with instant solutions

- 🎮 Matching games — gamified revision of key terms & concepts

- 📄 Study notes & PDFs — downloadable chapter material

- 🎥 Video classes on YouTube — subscribe to @learningsessions

💬 Want the full course? WhatsApp your course name to 8360944207 and our team will set you up.

📱 Study on the go — get our iOS & Android app at iibf.store/app.

Authoritative reference: Indian Institute of Banking & Finance (IIBF).

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.