Robotic Process Automation in Banking: CAIIB ITDB Guide (2026)

🤖 What Is Robotic Process Automation in Banking?

Robotic process automation in banking refers to software bots that replicate specific, rule-based human actions on a computer screen — logging into applications, copying data between systems, filling forms, and generating reports — without rewriting the bank's underlying IT systems. For CAIIB's Information Technology and Digital Banking elective, this is a high-yield topic because RPA sits at the intersection of legacy core banking platforms and the bank's need for speed, accuracy, and round-the-clock processing.

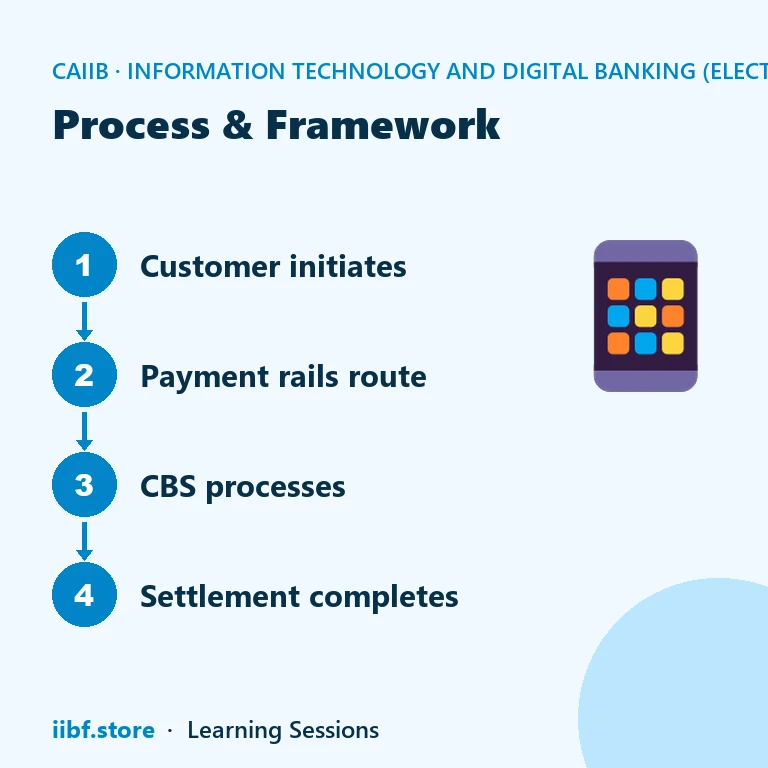

An RPA bot works the way a human clerk would: it opens the same application windows, reads the same screens, and keys data into the same fields. What changes is scale — the bot performs the task thousands of times a day with no fatigue and, when configured correctly, near-zero manual error. Candidates should understand that robotic process automation in banking automates the "doing" of a task, not the "deciding" — that distinction is exam-critical and separates RPA from AI-based decisioning systems.

The foundational concepts behind RPA build directly on topics covered under essentials of information technology, where system architecture, software layers, and application interfaces are introduced. Because most bots interact with applications over a bank's internal network, a working grasp of networking systems also helps candidates understand how bots authenticate, connect, and move data securely between servers during automated runs.

💡 Exam Tip: If a CAIIB question asks you to distinguish RPA from AI, remember: RPA follows pre-defined rules on structured data; AI/ML learns patterns and handles unstructured or judgment-based decisions. Many CAIIB ITDB questions test exactly this boundary.

⚙️ Core Components of an RPA Bot Architecture

A typical bank-grade RPA setup has four building blocks. The Recorder/Designer (often called "Studio") is where a developer records or scripts the sequence of steps a bot must follow — click here, read this field, paste there. The Bot Runner is the actual executable agent that carries out the recorded workflow on a virtual machine or desktop, either on a fixed schedule or on demand. The Orchestrator (Control Room) is the central console that schedules, monitors, logs, and manages every bot deployed across the bank's branches and back-office units — it is the single point from which IT and audit teams get visibility into what every bot did and when. Finally, credential and access management layers govern which systems a bot can log into, typically through a vault that stores service-account passwords separately from the bot script itself.

Robotic process automation in banking is generally classified into two deployment modes. Attended RPA bots sit on an employee's desktop and are triggered on demand to assist with a task in real time — for example, a branch officer clicking a button to auto-populate a loan application form. Unattended RPA bots run independently on servers, usually overnight or on a schedule, processing high-volume batch work such as reconciliations or report generation without any human present. Banks typically deploy a mix of both, matching the mode to the nature of the underlying process.

Understanding this component-level view matters for CAIIB because exam questions frequently test terminology — Orchestrator versus Bot Runner, attended versus unattended — rather than only conceptual definitions. Candidates who can map each term to its function in the automation pipeline answer these questions faster and more accurately.

🏦 RPA Use Cases Across Indian Banking Operations

RPA has been adopted widely across Indian public and private sector banks because it delivers fast, low-risk returns without touching core banking code. In back-office operations, bots are commonly used for NOSTRO/VOSTRO account reconciliation, matching thousands of transaction entries between internal ledgers and correspondent bank statements far faster than manual staff. In retail operations, bots extract data from KYC documents into account-opening workflows, validate PAN and Aadhaar formats, and populate core banking fields, cutting turnaround time for new account activation.

Compliance and reporting teams use RPA to auto-generate recurring regulatory and MIS reports — pulling data from multiple systems, formatting it to a prescribed template, and routing it for sign-off, all on a fixed schedule. Credit operations use bots for pre-sanction data collation, such as pulling CIBIL scores, financial statement figures, and collateral records into a single case file before a credit officer applies judgment. Loan servicing teams deploy bots to send standardised reminder communications, update EMI schedules after a part-payment, and reconcile suspense accounts.

Because RPA works at the presentation or API layer without altering source code, it is frequently the fastest way for a bank to digitise a manual process while a longer-term system upgrade is still being planned. This makes RPA a practical bridge technology rather than a replacement for core modernisation — a distinction examiners like to test through scenario-based questions.

⚠️ Common Mistake: Candidates often assume RPA "understands" the data it processes. It does not — RPA follows scripted steps on structured screens and breaks the moment a screen layout changes unexpectedly. This fragility is a key exam point on RPA limitations.

📊 Which Banking Processes Suit RPA?

Not every banking process is a good candidate for automation. The table below summarises the litmus test CAIIB candidates should apply: is the task repetitive and rule-based, and does it operate on structured, predictable data?

| Banking Process | Task Nature | Suitable for RPA? |

|---|---|---|

| NOSTRO/VOSTRO account reconciliation | Rule-based, structured data | ✅ Yes |

| Account-opening data entry from KYC forms | Rule-based, structured data | ✅ Yes |

| Complex credit underwriting with subjective judgment | Judgment-based, unstructured | ❌ No |

| Customer grievance resolution needing empathy/negotiation | Judgment-based, unstructured | ❌ No |

The pattern is consistent: wherever a human is essentially copying, checking, or moving data between systems in a predictable sequence, RPA delivers strong ROI. Wherever the task needs contextual judgment, negotiation, or handling of unstructured exceptions, RPA alone is the wrong tool — that is the domain of trained staff or, increasingly, AI-assisted decision support layered on top of RPA-collected data.

⚠️ Governance, Risks and Controls for RPA in Banks

Because RPA bots often run with the same system access as a human employee, they introduce a distinct set of operational risks that a bank's IT and audit functions must govern closely. The most cited risk is credential management: if bot login credentials are hardcoded into scripts or shared across multiple bots, it becomes difficult to maintain a clean audit trail of who (or what) performed a transaction, and a compromised bot account can be misused at scale. Banks address this through dedicated service accounts, credential vaulting, and mandatory periodic password rotation for every bot identity.

A second risk is process fragility — a bot that was built against one version of a screen can silently fail or, worse, post incorrect entries if the underlying application's layout changes without the automation team being informed. Banks mitigate this with exception-handling logic that halts a bot and alerts a human the moment an unexpected screen state appears, rather than letting the bot guess and proceed. A third governance requirement is maintaining a complete, centralised log of every bot run through the Orchestrator, since regulators and internal auditors treat bot actions with the same scrutiny as staff actions — every automated entry must be traceable to a specific bot, process, and timestamp.

Finally, banks must define a clear ownership model: a business process owner (not just the IT team) must sign off on what the bot is authorised to do, its transaction limits, and its escalation path, so that automation does not silently expand beyond its approved scope over time.

For exams, remember the three pillars of RPA governance as a set: credential control, exception handling with human fallback, and centralised audit logging through the Orchestrator.

RPA in banking also intersects with several adjacent digital-banking themes worth reading together. Bots frequently feed data into systems used for data analytics for fraud detection, since clean, bot-extracted transaction data improves the accuracy of downstream monitoring models. Many banks now run their Orchestrator and bot pools on cloud computing in banking infrastructure to scale bot capacity during peak periods such as month-end reconciliation. Some banks are also exploring how bot-verified data trails could eventually connect with blockchain in banking for tamper-proof transaction records, though this remains an emerging combination rather than mainstream practice. Candidates preparing for the risk side of digital transformation should also skim how automation-driven data feeds into market risk capital charge calculations, since faster, cleaner data pipelines directly improve the timeliness of risk reporting.

🧠 Practice MCQs: RPA in Banking

Q1. Which of the following best describes the primary characteristic of RPA bots in banking? (a) They use natural language understanding to make credit decisions (b) They mimic rule-based, repetitive human actions on the user interface of existing applications (c) They physically replace ATM hardware components (d) They require rewriting the bank's core banking system

Answer: (b) — RPA bots replicate structured, rule-based UI actions on existing applications without altering the core system's underlying code.

Q2. In RPA architecture, which component is responsible for scheduling, monitoring and managing the deployment of bots across a bank's IT environment? (a) Bot Runner (b) Orchestrator / Control Room (c) Recorder (d) Studio

Answer: (b) — The Orchestrator (Control Room) is the central console that schedules, monitors, and logs all bot activity across the bank.

Q3. Which banking process is LEAST suited for direct RPA implementation? (a) Reconciliation of NOSTRO/VOSTRO accounts (b) Data entry for account-opening forms (c) Complex, judgment-based credit underwriting requiring exceptions (d) Generation of standard MIS/regulatory reports

Answer: (c) — RPA suits structured, rule-based tasks; subjective, judgment-heavy underwriting decisions fall outside RPA's scope and need human or AI-assisted judgment.

Q4. What is "attended RPA" in the context of banking automation? (a) A bot that runs unsupervised on a server, triggered by a schedule (b) A bot that works alongside a human employee on their desktop, triggered on demand (c) A cloud-native bot requiring no human interaction at all (d) A bot restricted to back-office batch processing active only at night

Answer: (b) — Attended RPA bots run on an employee's desktop and are invoked on demand to assist with a live task, unlike unattended bots that run independently on a schedule.

Q5. Which of the following is a key operational risk specific to RPA bots that a bank's risk/audit team must monitor? (a) Bot credentials being hardcoded or shared, creating access-control and audit-trail gaps (b) Excessive server power consumption (c) Inability of bots to run outside business hours (d) Bots directly modifying the core banking system's source code

Answer: (a) — Poor credential hygiene for bot service accounts is a well-documented RPA risk, since shared or hardcoded credentials weaken accountability and audit trails.

Want chapter-wise mock tests with 100+ MCQs? Start practising free →

Frequently Asked Questions

Is robotic process automation in banking the same as artificial intelligence?

No. RPA follows pre-defined, rule-based scripts on structured data and does not learn or adapt. AI/ML systems, by contrast, learn patterns from data and can handle unstructured inputs and judgment-based decisions. Many modern banking platforms combine both — RPA to execute steps and AI to make the underlying decision.

Does RPA require changes to a bank's core banking system?

Generally no. RPA bots typically operate at the user-interface or API layer, interacting with existing applications exactly as a human employee would, without any modification to the core banking system's underlying source code. This is one of the main reasons banks favour RPA for quick automation wins.

What is the difference between attended and unattended RPA bots?

Attended bots run on an employee's desktop and are triggered on demand to assist with a task in real time, such as auto-filling a form during a customer interaction. Unattended bots run independently on servers on a fixed schedule, typically handling high-volume batch work like reconciliations or report generation without any human involvement.

Why is credential management considered a major RPA risk in banks?

Because RPA bots often log into systems using shared service-account credentials, poor credential hygiene — such as hardcoding passwords into a bot script — weakens the audit trail and creates access-control gaps. Banks mitigate this through credential vaulting, unique bot identities, and periodic password rotation, all of which are monitored by IT and internal audit.

Conclusion: Strengthen Your CAIIB ITDB Preparation

Robotic process automation in banking is a compact but exam-heavy topic: know the architecture (Recorder, Bot Runner, Orchestrator), the deployment modes (attended vs unattended), the process-selection criteria (rule-based and structured versus judgment-based), and the governance risks (credentials, fragility, audit logging). Together these four pillars cover the large majority of CAIIB ITDB questions on this subject, and the same framework transfers cleanly to case-study questions on any other automation topic in the elective.

Ready to test what you've learned? Attempt chapter-wise mock questions on the CAIIB course page or head straight to iibf.store/tests for full-length practice sets, and browse more elective-specific guides on the Information Technology and Digital Banking elective hub to keep building exam-day confidence.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.