Correspondent Banking, Nostro-Vostro and SWIFT: CAIIB BFM PDF

How does your bank pay a supplier in New York without having a single branch in the United States? The answer is correspondent banking — the network of Nostro and Vostro accounts, SWIFT messages and national payment systems that CAIIB BFM Module A tests relentlessly. Today's free revision pack distils this exact chapter into 20 one-liners and 20 true/false questions, and the videos below give you the visual version. Download the PDFs, watch the clips, and this chapter is done.

Download today's free CAIIB BFM revision PDFs

20 exam-ready one-liners and 20 true/false questions with answers from this chapter, in two branded PDFs by Learning Sessions.

Nostro, Vostro, Loro & Mirror Accounts · CAIIB BFM Quick Revision · Watch on YouTube

What correspondent banking really is

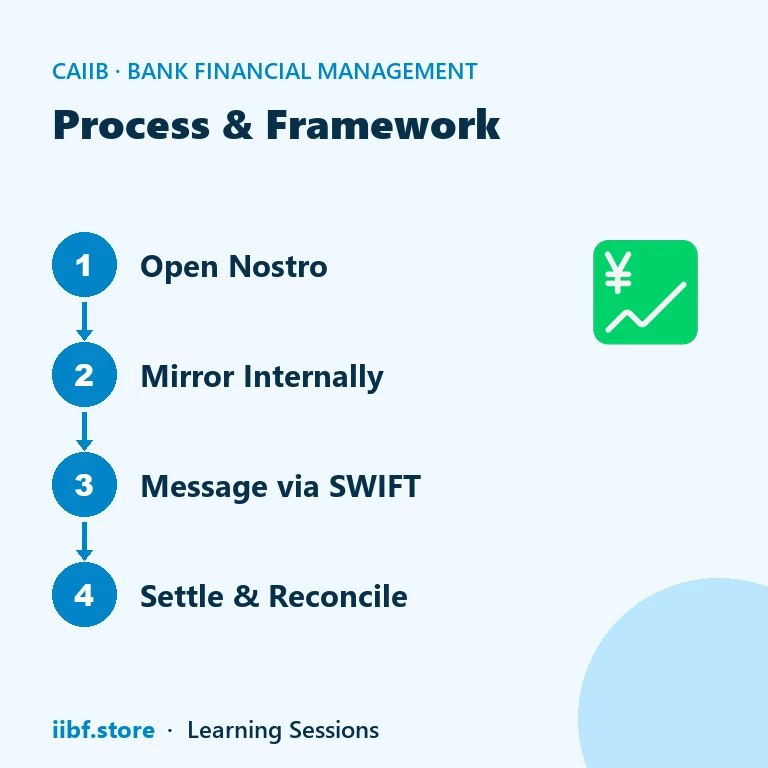

Correspondent banking is a relationship between two banks — not a branch arrangement — that lets a bank serve customers abroad without any physical presence there. Your bank in India appoints, say, a New York bank as its correspondent; that correspondent holds an account for your bank, executes dollar payments on its behalf and passes on messages through secure channels. It is the plumbing beneath every remittance, trade settlement and foreign-currency transfer in the BFM syllabus.

The account vocabulary is where examiners start. Nostro means "our account with you" — our bank's foreign-currency account held with a bank abroad. Vostro means "your account with us" — a foreign bank's rupee account held with us in India. A Loro account is "their account with them" — a third bank's account referred to in a transaction between two others. And a Mirror account is the internal shadow of a Nostro, maintained in two currencies (the foreign currency plus the home currency) so the bank can reconcile every entry. A newer exam favourite: the Special Rupee Vostro Account (SRVA), used to invoice and settle international trade in INR — and from May 2026 it can be opened without prior RBI approval.

SWIFT: messaging, not settlement

The single most repeated true/false in this chapter: SWIFT settles payments — false. SWIFT is a Brussels-based cooperative society that provides secure financial messaging only; it is not a clearing or settlement system. Actual settlement happens across Nostro/Vostro accounts and national payment systems. Counterparty authorisation on SWIFT now runs on the Relationship Management Application (RMA), successor to the Bilateral Key Exchange retired on 1 January 2009. And from November 2026 (operationally 14 November 2026), every SWIFT cross-border payment must carry a structured or hybrid postal address or face rejection — a fresh, very examinable update.

SWIFT & Global Payment Systems · CAIIB BFM Quick Revision · Watch on YouTube

Global and Indian payment systems: the comparison that wins marks

Once the correspondent banking accounts are in place, money actually moves through national large-value systems. BFM loves matching questions here, so learn this table as a set:

| System | Country/Zone | Type | One fact examiners test |

|---|---|---|---|

| Fedwire | USA | RTGS (Federal Reserve) | Operating since 1918 |

| CHIPS | USA | Private multilateral net settlement | Largest private-sector USD system, since 1970 |

| CHAPS | UK | Sterling large-value | Operated by the Bank of England |

| T2 | Eurozone | RTGS | Replaced TARGET2 on 20 March 2023, ISO 20022 |

| RTGS (India) | India | Real-time gross settlement | Min Rs 2 lakh, no cap, 24x7 since 14 Dec 2020 |

| NEFT (India) | India | Deferred net settlement | 48 half-hourly batches, 24x7 since 16 Dec 2019 |

Two India-specific updates worth flagging: Indian RTGS runs on a Y-model architecture, and from 1 April 2025 banks must let RTGS/NEFT remitters verify the beneficiary's name from the account number plus IFSC before sending, free of charge. Both appear in today's one-liners PDF with full explanations.

FEMA residency and NRI accounts: the chapter's second half

The same chapter folds in FEMA basics: a person resident outside India is one who stayed in India for 182 days or less during the preceding financial year, and an OCI registered for 5 years who has been ordinarily resident in India for 12 months may apply for citizenship. On the account side — NRE is INR-denominated, fully repatriable with tax-exempt interest; NRO repatriation is capped at USD 1 million per financial year per holder, post-tax; FCNR(B) runs 1–5 years in the deposit currency, so the depositor bears no exchange risk. We cover that trio in depth in our companion guide on NRE vs NRO accounts.

To make the chapter stick: download both PDFs above, watch the third video on correspondent banking made easy, then attempt a timed set on our CAIIB mock tests. Slot a revision block into your study planner, browse the full CAIIB course library, and cross-check any regulatory update on the RBI website before exam day.

How to revise this chapter in 20 minutes a day

Correspondent banking rewards spaced repetition more than marathon reading. Day one, learn the four account definitions and say them aloud in the Nostro-Vostro-Loro-Mirror order. Day two, add the SWIFT facts — cooperative society, Brussels, messaging only, RMA since 2009. Day three, drill the payment-systems table until Fedwire-1918 and CHIPS-1970 come without hesitation. Day four, attempt the true/false PDF cold and mark every miss. Day five, redo only the misses and take a ten-question timed set. Twenty focused minutes a day beats a three-hour Sunday session because the exam tests recall speed, not reading stamina — and the one-liners PDF above is deliberately built for exactly this loop.

Frequently asked questions

What is the easiest way to remember Nostro vs Vostro?

Think in Latin possessives: Nostro = "ours" (our account with you, held abroad in foreign currency); Vostro = "yours" (your account with us, held in India in rupees). Loro = "theirs", a third bank's account, and a Mirror account is our internal two-currency copy of the Nostro used for reconciliation.

Is SWIFT a payment or settlement system?

Neither. SWIFT only carries secure, standardised financial messages between banks. Settlement happens separately across correspondent banking accounts and national systems like Fedwire, CHAPS, T2 or Indian RTGS — which is precisely why this true/false appears in almost every BFM cycle.

What do the PDFs in this article contain?

Two free Learning Sessions PDFs for this exact chapter: one with 20 exam-style one-liners with short explanations, and one with 20 true/false questions with answers. They mirror the format IIBF actually tests and are ideal for a 15-minute daily revision loop.

What changed recently that I should quote in the exam?

Three updates: SRVA accounts can be opened without prior RBI approval from May 2026; SWIFT cross-border payments need structured or hybrid addresses from 14 November 2026; and beneficiary-name verification for RTGS/NEFT became mandatory and free from 1 April 2025.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.