NRE vs NRO Accounts: Differences That Matter for CAIIB BFM

If a customer moves abroad for a job, which account should their overseas salary sit in — and which one holds the rent they still earn from a flat back home? That single question is what the NRE vs NRO accounts topic in CAIIB BFM is really testing. The quick revision video below gives you the crisp version; this guide then locks in every distinction the examiner can throw at you, from repatriation to taxation to joint holding.

NRE vs NRO Accounts · CAIIB BFM Quick Revision · Watch on YouTube

NRE vs NRO accounts: the core idea in one line

The whole NRE vs NRO accounts distinction comes down to the source of the money. An NRE (Non-Resident External) account is meant for income earned outside India that a Non-Resident Indian wants to park in rupees back home. An NRO (Non-Resident Ordinary) account is meant for income earned inside India — rent, dividends, pension or a maturing domestic deposit. Fix that source rule in your head and most NRE vs NRO accounts questions answer themselves.

Both are rupee accounts opened by NRIs and PIOs under FEMA, and both can be savings, current, recurring or fixed deposits. What changes is how freely the money can leave the country and how it is taxed — and that is exactly where BFM likes to probe.

Repatriation and taxation: where the marks hide

Repatriation is the single biggest differentiator. Funds in an NRE account — both principal and interest — are freely and fully repatriable abroad. Funds in an NRO account face a ceiling: current-income interest is freely repatriable, but the balance can only be remitted up to USD 1 million per financial year, and only after applicable taxes are paid with the prescribed certification.

On taxation, the contrast is just as sharp. Interest earned on an NRE account is exempt from Indian income tax and there is no TDS. Interest on an NRO account is fully taxable in India and TDS is deducted at source, subject to any Double Taxation Avoidance Agreement relief. This tax-and-repatriation pairing is the classic NRE vs NRO accounts MCQ, so drill it until it is reflexive.

One more nuance the BFM paper enjoys: an NRE account can be held jointly with another NRI, or with a resident close relative on a "former or survivor" basis. An NRO account can be held jointly with residents on an "either or survivor" basis, which is why it doubles as the natural account for shared Indian income.

NRE vs NRO vs FCNR: the comparison table to memorise

| Feature | NRE Account | NRO Account | FCNR(B) Deposit |

|---|---|---|---|

| Purpose | Park foreign income in INR | Manage Indian income | Hold foreign currency |

| Currency | Indian Rupee | Indian Rupee | Foreign currency |

| Repatriation | Fully repatriable | Up to USD 1 mn/year | Fully repatriable |

| Interest taxable in India? | No (exempt) | Yes (TDS applies) | No (exempt) |

| Exchange-rate risk | Yes (INR) | Yes (INR) | No |

| Joint with resident? | Former or survivor | Either or survivor | Former or survivor |

Notice how FCNR(B) removes exchange-rate risk by keeping the deposit in foreign currency — a favourite trap when a question adds "the customer is worried about rupee depreciation." Work through a few of these scenarios on our CAIIB practice tests, revise the full syllabus inside the CAIIB course library, and build a repeat-revision slot into your study planner. The definitive rules sit in RBI's FEMA deposit regulations on the RBI website, and you can find more BFM revision guides across the iibf.store blog.

Five exam traps in NRE vs NRO questions

First, the funding trap: an NRE account can be funded from abroad or from another NRE/FCNR account, but rent received in India can never be credited to it — Indian income must flow to the NRO account. Second, the repatriation trap: the USD 1 million ceiling applies to NRO balances per financial year per account holder, not to NRE funds, which move freely. Third, the taxation trap: questions often say "interest on NRI deposits is exempt" — true only for NRE and FCNR(B), never for NRO. Fourth, the joint-holding trap: remember "former or survivor" for a resident relative joining an NRE account versus "either or survivor" on NRO. Fifth, the currency trap: both NRE and NRO are rupee accounts, so neither protects the depositor from exchange-rate movements — only FCNR(B) does that.

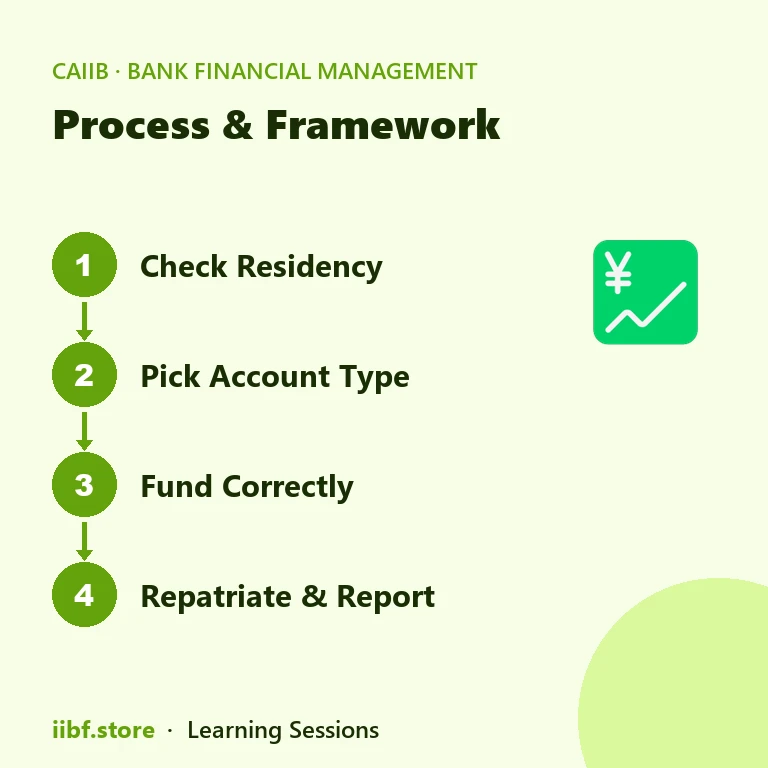

A quick scoring routine for the exam hall: read the question, identify where the money was earned, check which direction it needs to travel, and only then look at the options. Candidates who anchor on the source-of-funds rule solve NRE vs NRO accounts questions in under thirty seconds, leaving time for the numerical items elsewhere in the BFM paper. Practise this routine on a full-length mock at least twice before exam day, and note your error pattern — most aspirants miss the same trap repeatedly rather than five different ones.

Frequently asked questions

Can an NRI open both an NRE and an NRO account?

Yes. In fact most NRIs hold both — an NRE account for their overseas earnings and an NRO account for income that arises in India such as rent or dividends. The NRE vs NRO accounts choice is not either/or; it is about routing each rupee to the right account.

Which account is tax-free, NRE or NRO?

Interest on an NRE account is exempt from Indian income tax, while interest on an NRO account is fully taxable with TDS deducted at source. This is the most frequently tested single fact in the topic.

What happens to these accounts when the NRI returns to India?

On becoming a resident again, the NRE and NRO accounts must be redesignated as resident accounts (or, for foreign-currency needs, an RFC account). They cannot simply continue as NRI accounts once residential status changes under FEMA.

Is there any exchange-rate risk on an NRE account?

Yes. Because an NRE account is maintained in rupees, foreign income converted into it is exposed to rupee movements. An NRI who wants to avoid that risk entirely uses an FCNR(B) deposit, which stays in foreign currency.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.