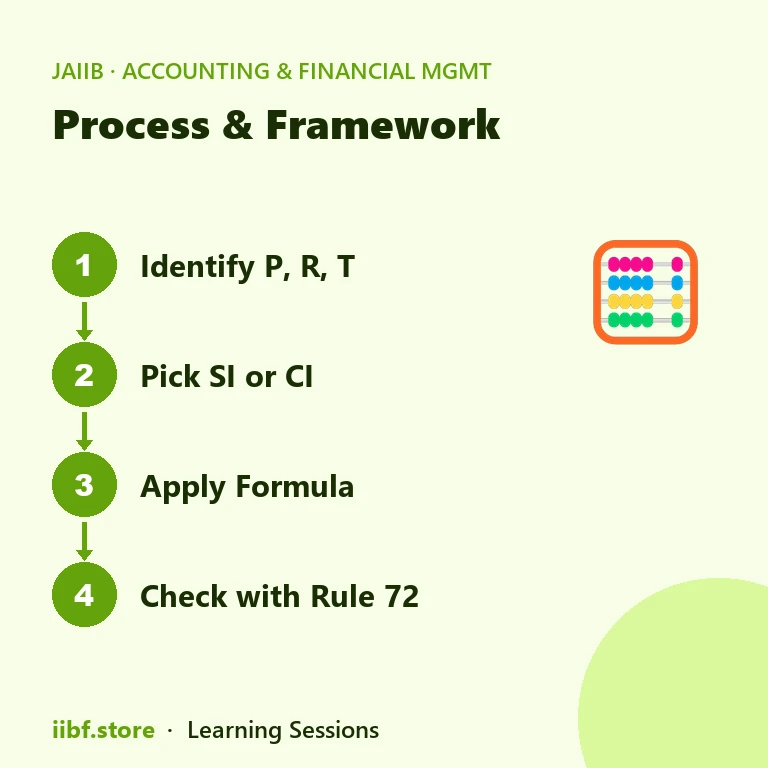

Simple and Compound Interest Formulas for JAIIB AFM + Free PDF

Almost every numerical mark in this JAIIB AFM chapter comes from just a handful of formulas — and every one of them starts with simple and compound interest. Today's free revision pack turns this exact chapter into 20 one-liners and 20 true/false questions you can finish with your morning tea. This guide walks through the formulas, the traps, and the newest RBI updates that examiners have already started asking, and both PDFs are yours to download below.

Download today's free JAIIB AFM revision PDFs

20 exam-ready one-liners and 20 true/false questions with answers on interest calculation, annuities and EMI — two branded PDFs by Learning Sessions.

Simple and compound interest: the two formulas everything builds on

Simple Interest is computed as SI = (P × R × T) / 100 on the original principal only — never on accumulated interest. Compound interest uses A = P × (1 + r/100)n, charging interest on principal plus accumulated interest, which is why FDs, RDs, loan amortisation and bond maths all live in compound territory. For the same principal, rate and period, compound interest is always at least equal to simple interest and exceeds it from the second period onward — a true/false that appears in nearly every JAIIB cycle.

Two extensions complete the picture. For compounding m times a year, A = P × (1 + r/(100 × m))m × n — and a higher m always gives a higher effective yield. At the limit sits continuous compounding, A = P × ert (with e ≈ 2.71828 and r in decimal form), which underpins Black-Scholes option pricing and several treasury models. And when you need a fast estimate, the Rule of 72 says money doubles in roughly 72 / r years under annual compounding — at 8%, about 9 years.

Fixed vs floating rates: where RBI rules enter the exam

A fixed rate stays constant for the entire tenure, while a floating rate resets periodically with its benchmark. Since 1 October 2019, new floating-rate personal, retail and Micro & Small Enterprise loans must be externally benchmarked (the EBLR regime), and floating-rate loans must reset at least once every 3 months. As per the June 2026 MPC, the Repo Rate stands at 5.25%, with SDF at 5.00% and MSF and Bank Rate at 5.50% — current figures examiners expect you to know. One more recent rule: under RBI's Pre-payment Charges Directions, 2025, floating-rate non-business loans to individuals carry no prepayment charge from any lender.

The chapter also distinguishes front-end interest (deducted upfront from the disbursed principal) from back-end interest (charged periodically on actual balances). Because front-end interest is computed on the gross amount, the effective rate always exceeds the nominal rate — a subtle point the true/false PDF drills twice.

Annuities, EMI and sinking funds: the calculation block

Once simple and compound interest are solid, the chapter layers on annuities. In an ordinary annuity payments fall at the end of each period; in an annuity due they fall at the beginning, making an annuity due worth (1+i) times its ordinary equivalent for both future and present value. The formulas to memorise:

| Concept | Formula | Typical exam use |

|---|---|---|

| Simple Interest | SI = P × R × T / 100 | Short-tenure deposits, quick MCQs |

| Compound Amount | A = P (1 + r/100)n | FD maturity values |

| FV of ordinary annuity | FV = C [((1+i)n − 1) / i] | RD maturity |

| PV of ordinary annuity | PV = C [(1 − (1+i)−n) / i] | Loan valuation |

| EMI | EMI = P r (1+r)n / [(1+r)n − 1] | Loan instalments |

| Sinking fund | C = FV × i / [(1+i)n − 1] | Bullet/balloon repayment build-up |

Remember the EMI behaviour question too: early instalments are interest-heavy and later ones principal-heavy, even though the instalment itself stays level. That single sentence has been worth a mark in multiple JAIIB papers.

How to use today's PDFs for maximum marks

Print or save both PDFs, then run a 15-minute loop: read the 20 one-liners once, attempt the 20 true/false cold, and re-read only the ones you missed. Repeat tomorrow before moving on. Numerical speed in AFM comes from daily contact with the formulas, not marathon sessions — the exam gives you roughly a minute per question, so the Rule of 72 style shortcuts in the one-liners PDF are genuine mark-savers.

Pair the PDFs with practice: attempt AFM numericals on our JAIIB mock tests, schedule the next revision pass in your study planner, and explore the full JAIIB course library for video lessons on every chapter. Current policy rates and interest-rate directions are always verifiable on the RBI website, and you'll find fresh daily revision drops on the iibf.store blog.

A worked example to lock the formulas in

Try this one from today's set: Rs 1,00,000 at 8% per annum for 2 years. Simple interest gives SI = 100000 × 8 × 2 / 100 = Rs 16,000. Compound interest (annual) gives A = 100000 × (1.08)² = Rs 1,16,640, so CI = Rs 16,640 — exactly Rs 640 more, which is the interest-on-interest for year two (8% of the first year's Rs 8,000). Now flip it with the Rule of 72: at 8%, the money doubles in about 72/8 = 9 years. If an option in the exam says "12 years", you can reject it instantly without touching a calculator. That is the level of fluency with simple and compound interest that the one-liners PDF is designed to build.

Frequently asked questions

What is the core difference between simple and compound interest?

Simple interest is charged only on the original principal for the whole tenure, while compound interest is charged on principal plus previously accumulated interest. Over any period beyond one compounding cycle, compound interest grows faster.

How accurate is the Rule of 72?

It is an approximation that works best for rates between roughly 6% and 10% under annual compounding. At 8%, it predicts doubling in 9 years, which is very close to the exact answer from the compound interest formula — good enough for one-mark MCQs.

Are the two PDFs in this article really free?

Yes. Both the 20 one-liners PDF and the 20 true/false PDF for this chapter are free Learning Sessions downloads — no sign-up needed. A new chapter drops daily, so bookmark the blog and collect the full set.

Which recent RBI changes from this chapter are most examinable?

Three: the EBLR external benchmarking regime for floating-rate loans (since 1 October 2019, quarterly resets), the Pre-payment Charges Directions 2025 removing prepayment charges on floating-rate non-business loans to individuals, and the current policy corridor — Repo 5.25%, SDF 5.00%, MSF/Bank Rate 5.50% as of the June 2026 MPC.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.