Capital Budgeting for JAIIB AFM: NPV, IRR and Payback Explained

For JAIIB AFM candidates, capital budgeting is the chapter that turns abstract accounting into real lending decisions. Every term loan a bank sanctions for plant, machinery, or expansion is, at heart, a capital budgeting exercise — will the future cash flows justify the money going out today? This guide breaks down the techniques, the exam traps, and how bankers apply capital budgeting when appraising borrower projects.

💰 What Is Capital Budgeting in Bank Lending

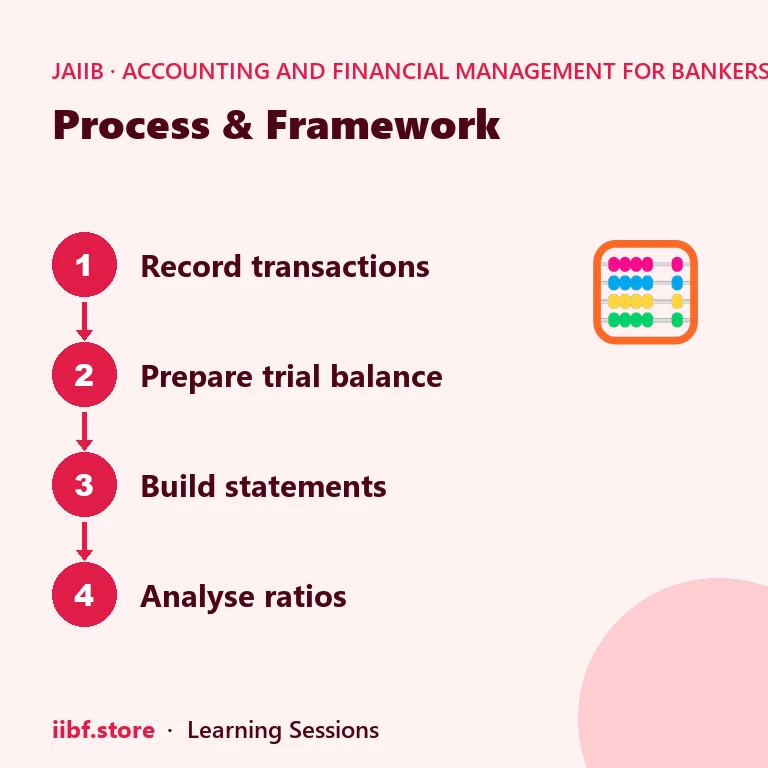

Capital budgeting is the process of evaluating long-term investment proposals — whether a firm should sink money into a new plant, a borrower should be sanctioned a term loan, or a bank should invest in its own infrastructure. Unlike day-to-day working-capital decisions, capital budgeting decisions are irreversible, capital-intensive, and stretch over many years, so the appraisal must account for the time value of money. For a bank credit officer, this is not an academic exercise: term loan appraisal, project finance, and infrastructure lending all lean on the same discounted cash flow logic taught in the DEFINITION SCOPE AND ACCOUNTING STANDARDS INCLUDING IND AS chapter, since projected financials must first be understood before they can be discounted. A borrower's projected profit-and-loss and balance sheet feed the cash flow estimates, and any weakness in the underlying accounting — inconsistent depreciation policy, aggressive revenue recognition — distorts the capital budgeting output before appraisal even begins. That is why AFM treats capital budgeting as the natural extension of financial statement analysis rather than a standalone formula set.

📊 Key Capital Budgeting Techniques Bankers Must Know

Five techniques dominate the JAIIB syllabus and real credit appraisal desks alike. The Payback Period simply measures how many years it takes to recover the initial outlay from net cash inflows — quick to compute but blind to what happens after payback and ignorant of the time value of money. The Accounting Rate of Return (ARR) uses average accounting profit over average investment, again without discounting. The three discounted techniques are where the real appraisal happens: Net Present Value (NPV) discounts all future cash inflows and outflows to today using the cost of capital and accepts the project if NPV is positive; Internal Rate of Return (IRR) finds the discount rate at which NPV becomes zero and compares it against the required rate of return; and the Profitability Index (PI) expresses the present value of inflows per rupee invested, useful when capital is rationed across competing proposals. NPV is generally preferred in theory because it directly measures value addition in rupee terms, while IRR is preferred by practitioners because percentage returns are easier to communicate to sanctioning committees.

🏦 Capital Budgeting vs Depreciation and Accounting Standards

A subtle but exam-favourite link is between capital budgeting and depreciation. Capital budgeting works on cash flows, not accounting profit, so depreciation — a non-cash charge — is added back to net profit after tax to arrive at operating cash flow. Yet depreciation is not irrelevant: it creates a tax shield, since higher depreciation lowers taxable income and therefore the cash tax outflow, which in turn raises the net cash inflow used in NPV and IRR calculations. This is precisely why the DEPRECIATION chapter and capital budgeting are examined together — a project appraisal question routinely asks candidates to add back depreciation before discounting cash flows. Bankers also cross-check the borrower's basic bookkeeping discipline covered in BASIC ACCOUNTANCY PROCEDURES before trusting projected figures, since sloppy ledger maintenance upstream means unreliable cash flow projections downstream. RBI's prudential lending framework, published at rbi.org.in, expects banks to document the appraisal methodology for term loans above threshold exposure, making NPV/IRR working papers part of the credit file, not just an academic footnote.

⚖️ Common Pitfalls Bankers Must Avoid in Appraisal

Three mistakes recur both in the exam hall and in real credit files. First, mixing up incremental cash flows with total cash flows — only the additional cash flows caused by the project should enter the calculation, not the firm's entire cash flow. Second, ignoring the mutually exclusive vs independent project distinction: when choosing between mutually exclusive projects, NPV ranking should drive the decision even if IRR ranks them differently, because IRR can mislead when project sizes or cash flow timing differ sharply. Third, using the wrong discount rate — the cost of capital (or the bank's benchmark lending rate plus risk premium) must reflect the risk of the specific project, not a generic company-wide rate. Getting the discount rate wrong understates or overstates NPV and can flip a lending decision entirely. Candidates should also watch for questions that combine capital budgeting with working-capital-linked ratios; understanding how a firm is currently leveraged, a topic covered in the debt-equity ratio guide, changes how much additional debt-funded capital expenditure a bank should comfortably sanction.

| Technique | Considers Time Value of Money | Output Format | Best Use Case |

|---|---|---|---|

| Payback Period | ❌ | Years | Quick liquidity screening |

| Accounting Rate of Return (ARR) | ❌ | Percentage | Simple profitability check |

| Net Present Value (NPV) | ✅ | Rupee value | Absolute value-addition decision |

| Internal Rate of Return (IRR) | ✅ | Percentage | Comparing against hurdle rate |

| Profitability Index (PI) | ✅ | Ratio | Ranking projects under capital rationing |

💡 Exam Tip: When NPV and IRR conflict on mutually exclusive projects, always go with the NPV decision — it directly measures rupee value created, which is the true wealth-maximisation objective.

🧮 Capital Budgeting, Funds Flow, and the Bigger AFM Picture

Capital budgeting decisions eventually show up in a firm's funds flow statement as a long-term application of funds, financed either through owned capital or borrowed term funds. A banker reviewing a borrower's funds flow statement alongside a capital budgeting proposal checks whether the financing pattern matches the FITL (funds indicating term loan) philosophy — long-term assets should ideally be financed by long-term sources, not short-term working capital limits. This cross-check protects both the bank and the borrower from an asset-liability mismatch. It also connects capital budgeting to macro variables: the discount rate used in NPV calculations is influenced by prevailing interest rates and inflation expectations, a theme explored in the types of inflation in India article — rising inflation typically pushes up the cost of capital and can turn a marginally positive NPV project negative. Bankers preparing sanction notes are expected to sensitise NPV/IRR outputs to a range of discount rates precisely for this reason, a practice examiners test through "what if the discount rate rises by 2%" style numerical questions.

⚠️ Common Mistake: Students often discount the accounting profit figure directly instead of first converting it to cash flow (adding back depreciation and adjusting for working capital changes) — this alone can cost 2-3 marks in a numerical question.

📌 Remember: IRR is the discount rate that makes NPV exactly zero — if you can compute NPV at two trial rates, interpolation gives you the IRR quickly in the exam.

🧠 Practice MCQs: Capital Budgeting

Q1. Which capital budgeting technique ignores the time value of money entirely? (a) Net Present Value (b) Internal Rate of Return (c) Payback Period (d) Profitability Index

Answer: (c) — Payback Period only measures the time to recover the initial investment and does not discount cash flows.

Q2. In NPV calculation, depreciation is added back to net profit after tax because: (a) it increases taxable income (b) it is a non-cash expense (c) it reduces the project's life (d) it is ignored by RBI

Answer: (b) — Depreciation is a non-cash book entry, so it is added back to arrive at actual operating cash flow.

Q3. When NPV and IRR give conflicting rankings for mutually exclusive projects, which should generally be preferred? (a) IRR (b) Payback Period (c) NPV (d) ARR

Answer: (c) — NPV is preferred because it measures absolute rupee value creation, aligned with the wealth-maximisation goal.

Q4. The Profitability Index (PI) is most useful when: (a) a firm has unlimited capital (b) capital is rationed across multiple projects (c) only payback matters (d) depreciation is nil

Answer: (b) — PI ranks projects by present value generated per rupee invested, ideal for capital rationing decisions.

Q5. IRR is defined as the discount rate at which: (a) payback period equals zero (b) NPV equals zero (c) ARR equals cost of capital (d) cash inflow equals cash outflow undiscounted

Answer: (b) — IRR is, by definition, the discount rate that makes the Net Present Value of a project exactly zero.

Want chapter-wise mock tests with 100+ MCQs? Start practising free →

Frequently Asked Questions on Capital Budgeting

Is capital budgeting only relevant for corporate finance, or does it matter for bank credit officers too?

It matters directly for bank credit officers — term loan appraisal, project finance sanctions, and infrastructure lending all use NPV/IRR-style capital budgeting logic to decide whether a borrower's project can service the proposed debt.

Why is NPV generally considered superior to IRR for decision-making?

NPV directly measures the absolute rupee value a project adds after discounting, and it does not suffer from the multiple-IRR or reinvestment-rate assumption problems that can distort IRR results for non-conventional cash flow patterns.

How does depreciation affect capital budgeting cash flows?

Depreciation itself is a non-cash expense so it is added back to profit after tax, but it lowers taxable income and creates a real tax-shield benefit, which increases the net cash inflow used in NPV and IRR calculations.

What discount rate should be used in NPV calculations for bank project appraisal?

The discount rate should reflect the project's specific risk and the bank's cost of capital or benchmark lending rate plus an appropriate risk premium, not a generic company-wide average rate.

Master every numerical variant of NPV, IRR, and payback with structured chapter notes and unlimited attempts — explore the AFM topic hub, revise related concepts like the ROCE, ROE and ROA and break-even analysis for bankers guides, then lock in your speed with full-length JAIIB AFM mock tests on iibf.store.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.