Skewness Explained Simply: CAIIB ABM Quick Revision 2026

Ask ten CAIIB candidates to define skewness and most will mumble something about a curve leaning to one side. That instinct is right — but the exam wants precision, not a mumble. Skewness is a small, high-yield topic in the CAIIB ABM statistics chapter, and a couple of minutes of clear thinking is enough to bag the mark every time. This quick revision breaks down what skewness means, the three types, the formula, and the mean–median–mode trick the examiner relies on.

Watch the short explainer below, then use the notes to cement the idea.

Skewness Explained Simply · CAIIB ABM Quick Revision · Watch on YouTube

What does skewness measure?

Skewness measures the asymmetry of a distribution — whether the data leans to the left or the right of the centre. A perfectly symmetrical distribution, like the ideal bell curve, has zero skewness: its left and right halves are mirror images. The moment one tail stretches out longer than the other, the distribution becomes skewed, and skewness puts a number on how much and in which direction.

Why does a banker care? Because most real financial data is skewed. Incomes, loan sizes, and account balances all cluster at the low end with a long tail of large values, giving a positive skew. Recognising skewness helps you interpret which average — mean, median, or mode — best represents a lopsided dataset.

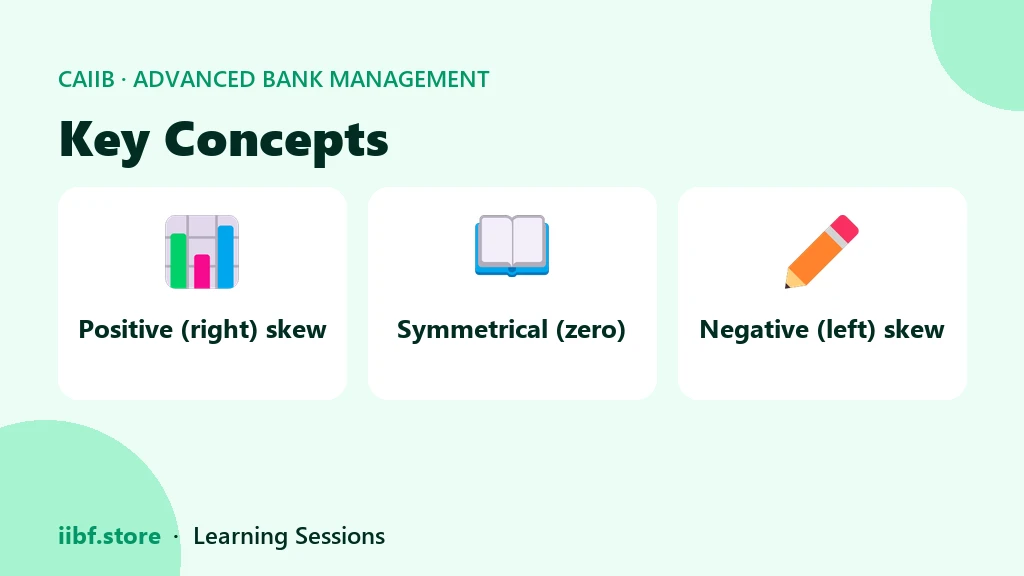

The three types of skewness

Every skewness MCQ boils down to identifying one of three cases. The key is the relationship between the mean, the median, and the mode.

| Type | Tail direction | Mean, Median, Mode order |

|---|---|---|

| Positive (right) skew | Long tail on the right | Mean > Median > Mode |

| Symmetrical (zero skew) | Both tails equal | Mean = Median = Mode |

| Negative (left) skew | Long tail on the left | Mean < Median < Mode |

The mnemonic that never fails: the mean is dragged towards the tail. In a positive skew the long tail is on the right, so the mean is pulled to the right, making it the largest of the three. Flip everything for a negative skew. If you remember only one thing about skewness, remember this.

The formula: Karl Pearson's coefficient

The most examined measure of skewness is Karl Pearson's coefficient of skewness:

Skewness = (Mean − Mode) ÷ Standard Deviation

When the mode is not clearly defined, the empirical version is used: Skewness = 3 × (Mean − Median) ÷ Standard Deviation. A positive result means positive skew, a negative result means negative skew, and zero means the distribution is symmetrical. The sign is what the exam usually tests, so always check whether the numerator is positive or negative before you read the options.

Worked example. A branch's loan data has a mean of 60, a mode of 48, and a standard deviation of 10. Skewness = (60 − 48) ÷ 10 = 12 ÷ 10 = +1.2. The positive sign confirms a right-skewed distribution — a long tail of large loans, exactly what you would expect.

How to lock skewness into memory before the exam

Skewness sits right next to kurtosis in the syllabus, and the two are frequently paired in a single question, so revise them together. Drill the mean–median–mode ordering until it is automatic, and practise a few coefficient calculations so the sign never trips you up. Reinforce the concept with our CAIIB mock tests, sharpen recall with the statistics match game, and study the complete chapter inside the Advanced Bank Management course. The definitions here follow the standard statistical treatment referenced by the Indian Institute of Banking & Finance.

Why skewness matters in real banking data

It is tempting to treat this topic as pure exam theory, but the shape of a distribution has real consequences for how a bank reads its numbers. Consider the average balance in a set of savings accounts. A handful of high-net-worth customers can lift the arithmetic mean far above what a typical account actually holds. A manager who quotes only the mean would badly overstate the “normal” customer — and the reason is right-side asymmetry in the data.

This is precisely where recognising the shape earns its keep. In a right-skewed dataset the median is usually the fairer summary, because it is not dragged around by a few extreme values the way the mean is. Loan sizes, transaction amounts, and branch-wise deposits almost always lean the same way, so a banker who instinctively reaches for the median when the data is lopsided will make better decisions than one who blindly reports the average.

The exam mirrors this real-world logic. When a question hands you a mean noticeably larger than the median, it is quietly telling you the distribution leans right, and the correct interpretation follows immediately. Train yourself to read those signals: compare the mean and median first, decide the direction of the lean, and only then evaluate the options. That habit turns a shape question from a guessing game into a two-second deduction, and it is exactly the kind of applied reasoning the Advanced Bank Management paper is designed to reward.

Frequently asked questions

What is positive skewness?

Positive skewness means the distribution has a long tail on the right side. In this case the mean is greater than the median, which is greater than the mode. Income and loan-size data are typically positively skewed.

What is the formula for skewness?

Karl Pearson's coefficient of skewness is (Mean − Mode) ÷ Standard Deviation. When the mode is ill-defined, the empirical form 3 × (Mean − Median) ÷ Standard Deviation is used instead.

How do mean, median and mode relate in a skewed distribution?

In a positive skew, Mean > Median > Mode. In a negative skew, Mean < Median < Mode. In a symmetrical distribution all three are equal. The mean is always pulled towards the longer tail.

What is the difference between skewness and kurtosis?

Skewness measures the asymmetry of a distribution — which way it leans. Kurtosis measures its peakedness and tail heaviness. Both describe shape but capture different features, and CAIIB ABM tests them together.

Quick quiz on this topic

5 exam-style questions from our free test bank — check yourself before you move on.

Practice this topic

Take a free mock test, download chapter PDFs, or watch a video class — all included on iibf.store.